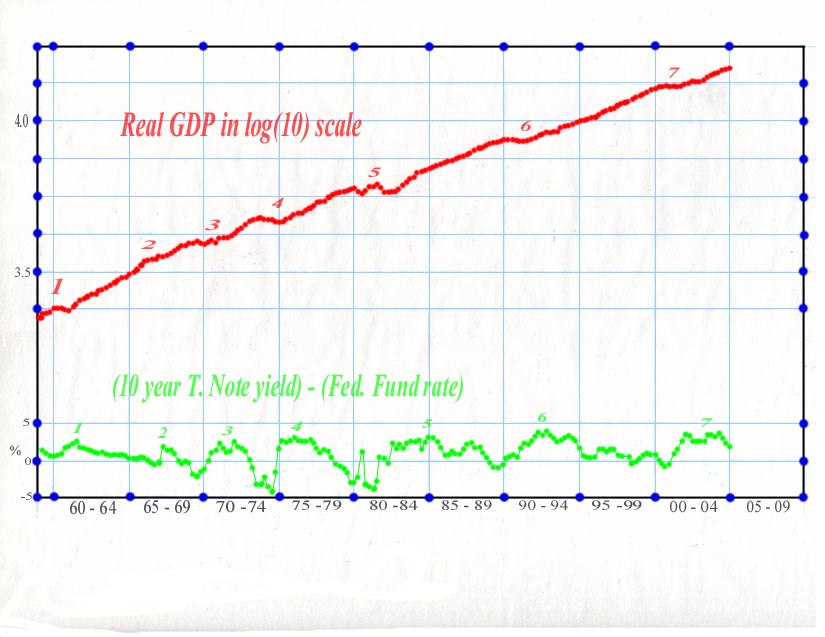

The word "conundrum" is frequently used to describe the refusal of long-term interest rates to follow the rising short-term interest rates. There are many speculations about the reason of this disparate behavior of interest rates. In this website we have also offered an explanation for the behavior of interest rates (see Comment 17). However, many are concerned not about the reason but about the consequence of this behavior of the long-term interest rates. Since the steady rise of the short-term interest rates, the yield difference between 10 year Treasury Note and the Federal Fund has shrunk to about 1 % from over 3 % a year ago. Some claim that when this yield difference becomes negative a recession will hit the economy. Others worry about the burst of the housing bubble when the long-term interest rates start to rise and the yield difference stops to shrink. The purpose of this comment is to investigate the consequence of this peculiar interest rate movement by directly looking into the relevant data themselves instead of doing idle speculations. In the following graph the real GDP of every quarter since 1959 is plotted in logarithmic scale as red points. The quarterly average of yield difference between 10-year T. Note and the Federal Fund is plotted as green dots.

In logarithmic scale, a straight segment of the real GDP data implies that the real GDP is growing with a constant rate. Thus we can immediately see the period of slow growth without relying on the artificial definition that two consecutive quarters of negative growth in GDP constitutes a recession. The period of economic slowdowns are marked from 1 to 7 on the red curve (real GDP) with 7 implying the most recent slow down associated with the burst of the "dot com" bubble. The peaks of the yield difference are also marked from 1 to 7 on the green curve. It is easy to see that the peaks of the yield difference curve are closely associated with the economic slowdowns of the red curve. A close inspection reveals that an economic slowdown comes first and then the yield difference curve will climb to a peak. This correlation between an economic slowdown and a peak of the yield difference curve is easy to explain. When The Federal Reserve Board (FED) notices an economic slowdown, it will start to lower the Federal Fund's rate. However, long-term interest rates are more resilient and are not controlled by FED directly. Thus long-term interest rates will not follow the rapidly falling Federal Fund's rate and the yield difference curve will start to climb. When the economy comes out of a recession, FED will keep the Federal Fund's rate steady, but the long-term interest rates will start to rise due to revived demand for money and thus the yield difference curve will continue to rise. As an economic recovery takes place and the yield difference curve reaches a peak or a plateau, the fear of overheating and the creeping inflationary pressure will prompt FED to raise the Federal Fund's rate. Since the long-term interest rates can not be commanded by FED as the short-term interest rates, the long-term rates will not rise as quickly as the short-term rates, and thus the yield difference curve will start to plunge. The first leg of the plunge of the yield difference curve is usually very steep, and will bring the yield difference curve to near zero or even to the negative territory if inflation pressure is great. Before the globalization process as indicated by the peaks 1 to 4 on the green curve, an economic slowdown will materialize at the end of this first leg of downturn of the yield difference curve. After the globalization scheme has taken hold as represented by the peaks 5 and 6, the first leg of down turn produces only a slight disturbance in the economic expansion. It takes more than one leg of down turns to bring in a full-scale economic slowdown. This fundamental change of the structure of American economy is due to the runaway trade deficit that causes a strong disinflationary trend and prolongs the economic expansion as has been pointed out in Article 1 and Article 2.

We are currently at the first leg of down turn from peak 7 on the green curve. Though the curve ends at the first quarter of 2005, the second quarter data will take the curve down to 1 % level. We cannot blindly follow the trend after the first down-legs associated with peaks 5 and 6, and consider this recent down-leg will have minimum effect on the economic growth of America, since the situation of globalization scheme has changed from the period of peaks 5 and 6. The change is due to the emergence of China as the defector proxy-exporter for many other countries. As has been pointed out in Comment 8 and Comment 10, China is still a developing economy that is by definition inefficient when it comes to the usage of raw materials. China's economy is heavily dependent on its export engine and the massive dollar buying operation. The booming Chinese domestic economy supported by its runaway export, and the expanding American economy supported by its runaway trade deficit are two sides of the same coin. Thus at the time of America's economic expansion, China's demand for raw material like oil also will expand rapidly. With its huge population, the demand from China will put a substantial strain on the commodity markets. The rapidly rising commodity prices in turn nullify the beneficial effect of the large trade deficit on the inflation front and FED is forced to keep interest higher for a longer period. Thus we expect that this leg of down-turn of the yield difference curve will have somewhat more severe effect on US economy than the cases after peaks 5 and 6; it will cause the economic growth to have a noticeable slow down, like down to 3 % growth rate for 2005, and even lower for 2006 as discussed in Projections for US economy .

We should note that FED is rising the Federal Fund's rate not only to fight the current monthly announced inflation rate but also to fight the future inflation threat. The most prominent future inflation threat is the collapse of Dollar. Thus we may view the major reason of FED's tighter monetary policy is to support Dollar as discussed in Comment 17. On the other hand the long-term interest rate is determined by the market perception of future inflation rates. With Dollar boosted by the rise of short-term interest rates the threat of inflation caused by the collapse of Dollar retreats, and thus long-term interest rates can stay low. This behavior of interest rates is pure "logic", not "conundrum". With those understandings we may draw the following scenario for the near-term course of American economy:

Dollar has experienced a sharp downturn against Japanese Yen, Taiwan Dollar and South Korean Won in the stretch from August, 2003 to March, 2004. During that period Euro has also continued to rise strongly against Dollar. With roughly two years of time-delay that weakness of Dollar is going to moderate the expansion of America's trade deficit around the end of 2005. We should note that Chinese Yuan has not participated in that Dollar devaluation at late 2003. With China as the largest contributor to America's trade deficit, US trade deficit near the end of 2005 will not have any significant drop, but just a hiccup in its steady expansion. That hiccup in the trade deficit will in turn show up as a slowdown in the growth of GDP. By the time when the above-mentioned hiccup in US trade deficit and economic growth shows up, the Federal Fund's rate will approach 4% and the yield difference will fall to near zero. This coincidence will prompt many to point their fingers at FED, arguing that it is FED's overzealous move to lift the Federal Fund's rate that is causing the weakness in American economy. Thus the pressure on FED to stop the tightening move will be very strong to the degree that FED will concur and abandon its short-term rate raising operation. This reversal of FED's policy will weaken Dollar vs. Yen and Euro. Also at that time the political pressure on Yuan to rise vs. Dollar will reach its paramount. Thus very likely Dollar will start a sharp dive against all those major currencies. This kind of sharp drop of the value of Dollar will weaken the confidence of long-term interest rate players about the future course of inflation in America. The long-term interest rate will rise and so will the yield-difference curve. This means that the first leg of down turn of the yield-difference curve will be over. The rise of long-term interest rates will curb the expansion of the real estate bubble, reduce the consumption power of American consumers that rely heavily on creative mortgage refinancing, and thus will usher in an even slower growth period for American economy. However, the real effect of the sharp drop of Dollar against all the major trading currencies including Chinese Yuan will only show up two years later, around the end of 2007, as a significantly reduced American trade deficit and a full-scale economic slowdown.

Note: This comment becomes an independent file to save the download time. If you want to navigate into other comments, either use the "back" button of your browser to return to the page where you come from, or Return to the Home Page of the Website