YEN/DOLLAR, TRADE DEFICITS, AND

RECENT BOOM BUST CYCLES OF USA

by

Chih Kwan Chen

(Aug. 17, 2003)

1. INTRODUCTION

Economic globalization has made trade

imbalances among economic powers of the world expand to a significant amount.

The major deficit country is The United States of America (abbreviated

as US), and the major surplus regions are Japan and other Pacific Rim Countries.

During the path of the economic globalization, that is, since 1982, US

had experienced two major boom bust cycles, the first boom topped at the

end of 1987 and the second boom peaked at the middle of 2000. A close inspection

has found that both boom bust cycles are closely related to the explosion

and the subsequent shrinkage of US trade deficits. Furthermore, evidence

indicates that the ebb and flow of US trade deficits are driven by Japanese

Yen/US Dollar exchange rates. The purpose of this article is to lay this

study out and then discuss the reasons why the new Yen/Dollar exchange

rate driven cycles emerge under the current scheme of economic globalization.

Finally a warning is given to the impending total collapse of the world

economic order if the run away trade imbalances are not corrected.

Many economic analysts and commentators,

and some elementary economics textbooks attribute the effect of merchandise

trade balances on Gross Domestic Product (GDP) simplistically as "trade

surplus adds to and trade deficit subtracts away from GDP." According to

this line of logic, more positive trade balance, either less trade deficit

or more trade surplus, should be correlated with higher growth rate of

real GDP and vise versa. Another group of opinion frequently appear on

financial media is that in an economic boom people become more affluent

and want more luxurious life style, thus import more foreign made luxury

goods; on the other hand domestically produced luxury goods will be consumed

more domestically and will be exported less. This two effects cause the

merchandise trade balance to move toward negative direction. When the economy

is in a slump, less demand for imported foreign luxury goods and more room

to export domestically made luxury goods, thus more positive the trade

balance becomes. This second line of opinion leads to the conclusion that

faster growth in GDP should coincide with more negative trade balances

and vice versa, thus in total contradiction with the first kind of simplistic

explanation. In the next section the economic data (Ref. 1) for the

pre globalization era (from 1930 to 1981) are analyzed, and the result

supports the second line of thinking, which we call the theory of "cyclical

pattern of trade balances."

In Section 3, the study of the

economic data is extended to the current globalization period with the

emphasis put on the correlation between Japanese Yen/US Dollar exchange

rate and US merchandise trade deficit. It is found that Yen/Dollar exchange

rate leads US trade deficit by two years. The running account of why major

trend changes in Yen/Dollar exchange rate have occurred and how the changes

have been translated into the trend changes in US merchandise trade deficit

is given for the whole globalization era. Section 4 is devoted to the empirical

study of the relation between economic growth and trade balance for the

globalization era. A new phenomenon called "bridge" is observed and it

is pointed out that the bridge accurately indicates the beginning and the

end of a boom, or a bubble.

Sections 5, 6, 7 and 8 are for

the theoretical explanations of the new trade pattern. Section 5 is devoted

to the discussion how GDP report compiles trade data and why the simplistic

explanation of the effect of trade balances, that is, trade surplus adds

to GDP and trade deficit subtracts away from GDP, is not correct. In section

6 and 7 the impacts of imports and exports on the economic growth are studied

respectively. Section 8 is for some other theoretical considerations, like

why Yen/Dollar exchange rate leads US trade deficit by two years, and how

the bridge phenomena are related to economic booms and stock market bubbles.

In the final section, how the current

global economic order will unravel if the problem of huge trade imbalances

is not addressed soon is discussed.

2. PRE GLOBALIZATION ERA; 1930 - 1981

To study the relation between the

trade balances and

the economic growth, we use a correlation graph. The

vertical axis of the graph represents the annual percentage

change of real (inflation adjusted) GDP, and the horizontal

axis of the graph represents the ratio of a year's merchandise

trade deficit over the current dollar GDP of that year. Fig. 1

is such a graph covering the year 1930 to 1947. For

example, the growth rate of the real GDP of 1930 is -8.6%

and the ratio of merchandise trade surplus over the GDP of

1930 is 0.88%, so an open circle with a tag "30" is plotted

at the corresponding position in Fig 1.

Open circles in Fig. 1 are for

years 1930 to 1933. Here

we see the onset of the great depression with the real GDP

shrinking year after year and most severely in 1932. As the line "A"

shows, there is an anti correlation between

the economic growth and the merchandise trade balance, just as the

theory of cyclical trade balance pattern anticipated. Years 1934 to 1938

are represented by "X" 's. The data points of 1934 to 1937 shows the effect

of the "New Deal", that is,

large government spending had boosted the economic growth. There is

no clear correlation between the economic growth and the trade balance

during those artificially boosted years. However, as the data point of

1938 shows, the boosting effect of the "New Deal" was exhausted by 1938,

US economy had fallen back into the depression, and trade surplus expanded

substantially, again as the theory of cyclical trade balance pattern predicts.

The "H" 's in Fig. 1 represent

the years of 1939 to 1943, the years of the War. The phase of the European

War started in 1939, and US plunged into the World War II in 1940. The

resulting increased production of war related material and the price control

had really pushed up the economic growth, but we can still see the anti

correlation pattern between the growth rate and the trade balance. This

anti correlation in the war years can easily be explained by replacing

the words "luxury goods" in the theory of cyclical trade balance pattern

by the words "resources to produce war material". In the time of stepped

up production of war material, along with higher economic growth rates,

US imported more raw material for the production of weapons, and thus more

negative the merchandise trade balance became. The year 1944 to 1947 are

represented by black circles in Fig. 1. The production of war material

peaked in 1943, and thus the drop of the growth rate in 1944. The World

War II ended in 1945. The economic growth plunged precipitously due to

the stoppage of production of weapons, and the trade balance turned sharply

positive due to the reduction of import of raw material needed for the

weapon production. However, US was the only major economic region not scorched

directly by the war. As the rebuilding efforts in Europe and Asia took

hold, US became the factory of the world to supply the needed material

to Europe and Asia, and this push of export had employed idled capital

and labor and had slowed down the plunge of economic growth in 1947.

From the study of Fig. 1, we only

see one positive correlation between the economic growth and the trade

balance in 1946 to 1947 which happened in a distressed situation, but witness

numerous occasions of anti correlation between the economic growth and

the trade balance; this is a clear rebuff of the simplistic explanation

that trade surplus adds to and trade deficit subtracts away from GDP; in

all the later years we will see this kind of anti correlation relation

appear repeatedly. The ratio of trade balance to GDP is limited to the

range of -0.2% to 1.2%, except two abnormal years 1946 and 1947 as

discussed before. It is the GDP growth rates that are pushed up and down

widely by various events, like the great depression, New Deal, the plunge

into the war and the ending of the war. As the economy jumps into a new

phase according to the push and pull of those events, the anti correlation

between the growth and trade balance is visible within each phase of the

economic environment as the theory of cyclical trade balance pattern predicts.

In the years covered by Fig.1 we can confidently say that drastic events

were driving the economic growth rates, and in turn the economic growth

rates were more or less determining the trade balances within each phase

as the theory of cyclical trade pattern indicates.

Fig. 2 is for the years from 1948

to 1981.

The open circles represent data for the years

from 1948 to 1966. The line labeled "A"

indicates the existence of an anti correlation

relation between the growth rate of real GDP

and the ratio of merchandise trade balance over

the total amount of GDP. There were two

exceptional years, 1954 and 1958 that are

located far away from the line "A", but rather

fit well into the next phase of line "B". The reason

of large deviation in those two recession years

and why they fit well into line "B" will not be

analyzed here. The "X" 's represent years from

1967 to 1976. The line labeled as "B" represent

the anti correlation line of this phase. This period

was plagued by the malaise of Vietnam War, and

seems that was the reason of economic phase

transition from "A" to "B". In the phase "B" there is an exceptional

year 1974, that was the year of the first oil shock. US Trade balance deteriorated

and the economy went into a recession due to the spiraling oil price. However,

after the oil shock, the economy had moved back to the phase "B". The black

circles are the years of 1977 to 1981, the time of the second oil crises

and very high inflation rate in US due to irresponsible monetary policies

of Carter administration. The line "C" is the anti correlation line of

this phase. The remarkable feature of this phase is that the data points

are so well collimated along the line "C". It is also interesting to note

that the aberration year, 1974, of phase "B" rather fits well into phase

"C".

In Fig. 2, the growth rates of

real GDP are limited to the range of +9% to -1% for all three phases. It

is rather the trade balances that distinguish those phases. The anti correlation

lines "A", "B", and "C" are persistently shifting toward the left, in the

direction of negative trade balances. Since the major factor in defining

economic phases is the trade balances, not the growth rate as in Fig. 1,

we are not sure that the anti correlation lines in Fig. 2 are the result

of the theory of cyclical trade balance pattern; it is also possible that

it is the trade balances that were determining economic growth rates rather

than the other way around as in the theory of cyclical trade balance pattern.

However, we have not found any convincing source that had driven trade

balances during the period of Fig. 2. Therefore, for convenience we still

refer the anti correlation lines of Fig. 2 as those of the theory of cyclical

trade balance pattern.

3. GLOBALIZATION, TRADE DEFICITS AND YEN/DOLLAR EXCHANGE RATES

The economic globalization under

consideration is an environment within which merchandise trade barriers

have been steadily eliminated to allow unprecedented growth in the amount

of merchandise trades. The exchange rates among the major currencies of

the world are allowed to float, though the currency markets free from government

intervention are far from reality. The economic phase marked by line "C"

in Fig. 2 can be considered as the transitional period for the world to

enter this stage of economic globalization. It is not possible to

pick one firm date and say that from that date on it is the age of globalization.

However, for the convenience of discussion we choose 1982 as the start

of economic globalization; the reason of this choice will be made clear

soon.

The marked phenomena in the process

of the economic globalization are the explosive

expansions of US merchandise trade deficits

and the matching striking accumulation of

merchandise trade surpluses of Japan and other

Asia Pacific Rim Countries. A close inspection

reveals that US merchandise trade deficit is

driven by the Japanese Yen/US Dollar exchange

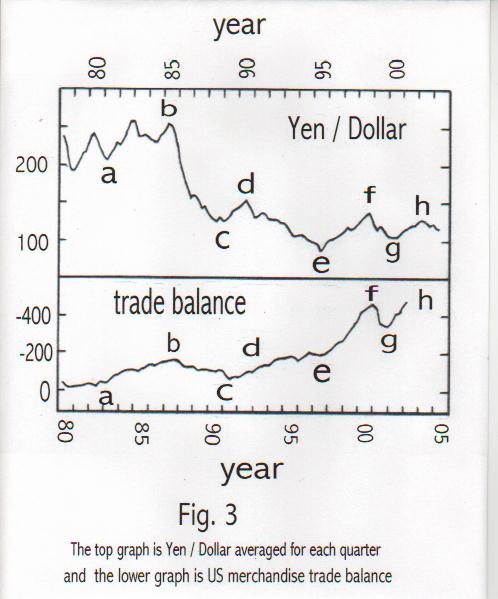

rates. In Fig. 3 annualized US merchandise trade

deficits are plotted for quarterly interval in the

bottom half of the graph. The minus sign in front

of the numbers along the vertical axis is to

emphasize that those numbers represent deficits.

The horizontal axis displays the years, starting at

1980. In the top half of Fig. 3 quarterly averages

of Japanese Yen/US Dollar are plotted, but with

the time scale on the horizontal axis shifted by two

years to the right. Thus the Yen/Dollar graph starts

at 1978. The major landmark points on both graphs

are marked by "a", "b", ... "h".

We will not discuss small wiggling

features of both graphs in this article, but only look at the gross characters

of both graphs. There is a remarkable matching of tops and valleys of the

two graphs except the stretch from "d" to "e"; the reason of this anomaly

will be discussed later on. This coincidence between two graphs indicates

that the ups and downs of US merchandise trade deficits are mainly driven

by Yen/Dollar exchange rates since the event in the top graph happens two

years before the corresponding events in the bottom graph. For example

the strong Dollar vs. Yen from 1981 to 1985, marked by "a" to "b" in the

top graph translated into expanding US merchandise trade deficit from 1983

to 1987, marked by "a" to "b" in the bottom graph, and so on.

Before going back to the correlation

graph as we did in Fig. 1 and Fig. 2, let us go through the events according

to the marked points in Fig. 3. First we will scan through the movements

of Yen/Dollar before the times of Fig. 3. Japanese Yen was released from

the fixed rate, 360 Yen/Dollar, at the beginning of 1970's and was allowed

to float. The market rate immediately followed the exchange rate at the

black market and US Dollar fell quickly against Yen; the Yen/Dollar rate

dropped to 265 Yen/Dollar by 1973. Then the first oil crises arrived in

1974. Japan must import almost all of its oil from outside and was especially

hard hit. Reflecting the crises and the worse situation of Japan, Yen had

fallen back to around 300 Yen/Dollar. Carter administration took office

in 1987, and started a very expansive monetary policy, inviting a substantial

inflation. That was the reason why Dollar fell, starting at 1977, from

300 Yen/Dollar to 200 Yen/Dollar by the end of 1978. Paul Vocker as the

chairman of the Federal Reserve System, used the strategy of "whatever

interest rates are necessary" approach to crash the nearly run away inflation.

As the result Dollar rose against Yen. The tail of the big Dollar fall

in Carter year due to the high inflation and the Paul Vocker recovery of

Dollar are registered in the top graph of Fig. 3 as the leftmost dip and

the subsequent rise. In 1980, due to the fall of Shaw of Iran, Dollar fell

again to the point marked "a" in the top graph of Fig. 3. Through this

rather complicated and significant falls and rises of Dollar vs. Yen, US

merchandise trade deficit displayed no significant movements. The phase

transition from "B" to "C" with worsening US trade balance actually occurred

at the time when Dollar fell big against Yen. Apparently the age of globalization

had not yet dawned.

Reagan Administration took office

in 1981. At that time the American hostages held in Iran were released.

The administration pursued "both butter and gun" policy, and made the budget

deficit explode. However, Reagan Administration had insisted to finance

the huge budget deficits through the issuance of treasury securities, not

like the previous administration to just print money to cover the deficits.

Thus the long term interest rates were pushed very high at the time when

US inflation was under control; this meant that inflation adjusted real

long term interest rates in US were sustained at a very high level for

a long time. Those conditions were the fertile ground for the appreciation

of US Dollar, and so Dollar rose against Yen as shown in the top curve

of Fig. 3 from point "a" to "b". Reagan administration also started economic

globalization by negotiating a series of tariff reducing agreements. The

strong Dollar coupled with the substantially liberalized trade environment

meant that the gate was open for Japanese goods to flood the US market,

and US merchandise trade deficit exploded, with two years of time delay

from the movement of Yen/Dollar rate, as shown in the section "a" to "b"

of the lower graph of Fig. 3.

By 1985, the explosion of US merchandise

trade deficit was unmistakable, and the currency market was ready to reverse

the trend of strong Dollar to punish the imprudent behavior of running

huge trade imbalances. Also by that time, the flood of Japanese goods had

hit very hard the heavy industrious regions of US, like the Midwest, causing

frequent uttering of the phrase "rust belt" on US media; the political

pressure on Reagan Administration to do something became unbearable. Finally

in 1985, a multinational meeting was called and two strategies were decided:

(1) To upward revaluate Yen. (2) For Japanese Government to stimulate the

domestic economy to lessen the pressure of US merchandise trade deficit.

The subsequent coordinated intervention by US and Japanese Governments

in currency market became the first stone to reverse the direction of strong

Dollar, and US Dollar started a long slide as depicted in the portion of

"b" to "c" in the top graph of Fig. 3. This sharp reversal of the Yen/Dollar

exchange rate again took two years to be translated into the trend change

of US merchandise trade deficit, and it was at the latter half of 1987

that US merchandise trade deficit finally peaked and started to decline.

Sensing this sea change in the trend of US merchandise trade deficit, US

stock market panicked in October of 1987 and thus that infamous October

disaster of 1987. The reason why stock market should have panicked as the

trend of merchandise trade deficit changed will be discussed in a later

section.

The 1987 stock market crash had

brought to the end the bubble of corporate raiders, mergers and acquisitions,

and junk bond financing. The currency market, sensing the coming period

of shrinking US merchandise trade deficit, bid up the Dollar vs. Yen as

shown in the section "c" to "d" in the upper graph of Fig. 3. This rise

of Dollar reversed the declining trend of US merchandise trade deficit

two years later as shown in the section "c" to "d" in the lower graph of

Fig. 3. During this time range in the globalization scene there occurred

a new phenomenon, that is, the emergency of Taiwan as the proxy exporter

of Japan. The sharp upward revaluation of Yen had made the manufacturing

of not so sophisticated products not cost effective in Japan, so many Japanese

manufacturers moved their factory to Taiwan to use low cost labors there

to produce those goods. Since Taiwan's currency was tagged to the US Dollar,

the cost of production of those goods was not affected by the strength

of Yen. When US trade deficit started to climb again in 1991 due to the

influence of stronger Dollar started in 1989, Taiwan was ready to play

a major role as the proxy exporter of Japan. On top of this Taiwan effect,

direct export from Japan also increased due to the strong Dollar. Those

two factors made US trade deficit rise rapidly again as shown in the portion

from "c" to "d" in the lower graph of Fig. 3.

In 1987 long promised Japanese

monetary stimulation started to have effect. In couple with the retreating

Japanese trade surplus due to the sharply higher Japanese Yen, the trend

of which started in 1985, Japanese domestic spending had started to explode.

However, either based on the erroneous simplistic thinking about trade

surplus and deficit that is already discredited in the previous section,

or bent to the domestic political pressure, Japanese Government refused

to take down trade barriers against inexpensive imports from manufactured

goods to agricultural products. As the result Japanese could only direct

abundant money into one direction, the speculation on "land"; thus the

infamous Japanese land bubble had developed. Also at that time Japanese

manufacturers had started to export equipment and industrial raw materials

to Taiwan to make it a proxy exporter of Japan. This new type of export

of Japan compensated the falling direct exports to US due to very strong

Yen, and as the result the decrease of Japanese trade surplus quickly stalled.

By 1990 this new reality became so obvious, and the currency market realized

that the sharp revaluation of Yen from 1985 was not enough to bring Japan

to correct its huge trade surplus, thus another wave to push Yen up and

US Dollar down had started and continued until 1995, shown in the section

from "d" to "e" in the top graph of Fig. 3. The strategy to use Taiwan

as the proxy exporter turned out to be an enormous success and the export

from Taiwan to US exploded. Also the flow of goods from Taiwan was resistant

to strong Yen since Taiwan's currency was fixed against US Dollar at that

time. Thus in spite of the sharp increase in the value of Yen in the stretch

of "d" to "e", US Trade deficit increase was not easy to reverse. Only

at the end of the move of Yen/Dollar in the "d" to "e" section, with the

2 year delayed effect, US trade deficit started to level off as is clear

from "d" to "e" in the bottom graph of Fig. 3. As Taiwan became more

affluent by serving as the proxy exporter of Japan, people became more

outspoken in human rights, democracy, free labor movement and environmental

control; multinational manufacturers abandoned Taiwan and migrated to other

Pacific Rim Countries in search of places with lower labor costs and the

freedom to pollute the environment. During the process of "d" to "e" it

was a tug of war between the currency market that wanted to devaluate Dollar

against Yen to correct the imbalances of trades and the multinational manufacturers

that expanded the proxy exporters to nullify the intent of the currency

market to correct lopsided trade imbalances.

By the beginning of 1995, Dollar

was dropping very rapidly against Yen, and US trade deficit had started

to level off. The currency market was as if saying, "Yen/Dollar will be

dropped to whatever level is necessary to correct the trade imbalance with

US at one side and Japan and the proxy exporters at the other side." Japanese

Government panicked at the thought that Japan's huge trade surplus would

melt away, so it started an unprecedented and risky gamble, that is, to

flood the market with Yen and thus to destroy the value of Yen deliberately.

Clinton administration was worried about the first signs of stagnating

economy as US trade deficit started to level off just before the reelection

campaign of 1996, so it explicitly endorsed the gamble of Japanese Government

under the catch phrase of "strong Dollar policy". Thus the sharp upturn

of Dollar vs. Yen as seen in the section of "e" to "f" in the Yen/Dollar

graph of Fig. 3. This currency movement of 1995 was translated into a further

rapid climb of US trade deficit as shown in the section from "e" to "f"

of the trade balance graph of Fig. 3. During this currency manipulation

which is still continuing today, the currency market knows that Japanese

Government, in principle, can issue whatever amount of Yen which is necessary

and dump on the market to push the value of Yen down, so no currency trader

will stand in the way of Japanese Government. Instead the currency market

used its ultimate weapon against the manipulator, that is, as if to say,

"All right, if you want weak Yen, we will give you weak Yen and much more

until you cry out from the pain of disaster sawed by yourself." Thus with

Japanese Government leading, and currency traders pushing, Dollar steadily

advanced against Yen, US trade deficit had exploded along with the trade

surplus of Japan, US economy sustained high growth rates accompanied by

Clinton's land slide victory in 1996, and Japanese economy turned to recession

from stagnation under the weight of run away trade surplus. Then the proxy

exporters became the first major innocent victims of this currency manipulation

in the form of Asian economic crises. The currencies of those proxy exporters

were tagged to US Dollar. As the value of Dollar moved up, so were the

currencies of those proxy exporters. Very soon those proxy exporters stopped

to function as proxy exporters, and Japan resumed to export directly to

US. Since those ex-proxy exporters were too slow to detach their currency

hookup to US Dollar, hot money flew in to take advantage of interest rate

differences between their treasuries and the US treasuries based on the

false assumption that the currencies of the ex-proxy exporters could be

tagged to Dollar for a long time. Those ex-proxy exporters experienced

consumption booms due to the influx of hot money, and ran trade deficits

just like US but against a much shallower asset base. When someone shouted,

"The Emperor has no cloth", all the hot money ran to the exit at once,

and thus triggered the Asian economic crises. The crises had boomeranged

back to Japan and turned a recession into a minor depression. The details

of this Asian economic crises is analyzed in other places so will not be

repeated here (Ref. 2 reflects the author's view that the main instigator

of the crises is the currency market manipulation of Japanese Government,

Ref. 3 is a more conventional view which assigns blame on the infrastructures

of Asia Pacific Countries other than Japan and argue somehow those infrastructures

of many countries failed simultaneously.) Even with the Asian economic

crises Japanese Government had insisted on to manipulate the currency market

to destroy the value of Yen, so currency traders helped Japanese Government

to push the value of Dollar higher and higher. By 1998 the currency crises

based on the increasingly strong Dollar had spread to non Asian currencies

pegged to the US Dollar. Both Japanese Government and US Government panicked,

and engaged a coordinated intervention to brake the trend of rising Dollar.

That was the signal that the currency market was waiting for, the signal

that the manipulator had cried out from the pain of the wound opened by

itself, so the currency market pushed Dollar off a cliff. That is the first

leg of the drop recorded in the section of "f" to "g" in Yen/Dollar graph

of Fig. 3. As the currency crises spread further, another sharp drop of

Dollar in 1999 as the second leg of drop of Yen/Dollar, shown in the section

"f" to "g" in Yen/Dollar graph of Fig. 3. This sharp reversal of the fortune

of US Dollar had been translated into, with almost a two year delay, the

reversal of the rapid increase of US trade deficit in the middle of 2000

as depicted in the portion of "f" to "g" of the trade balance graph of

Fig. 3. That trend reversal in the US trade deficit then had punctuated

the bubble of US stock market.

Japanese Government, without learning

from their disastrous currency market manipulation, started another round

of Yen destruction activity at the end of 2000, apparently taking advantage

of a political power vacuum in US due to the transition from Clinton to

Bush Administration, and is recorded in the Yen/Dollar curve of Fig. 3

as the section from "g" to "h". This push up phase ended in the spring

of 2002 due to the sharp market reaction. With almost the delay of one

and one half years, US trade deficit has risen sharply again in 2002 and

will peak out near the end of 2003 or the beginning of 2004 as can be seen

in the portion from "g" to "h" in the trade balance curve of Fig. 3.

4. CORRELATION BETWEEN ECONOMIC GROWTH AND

TRADE DEFICIT IN THE GLOBALIZATION ERA

In the previous section we have

shown that the graph of Yen/Dollar rates shifted two years toward the right

direction coincides remarkably with the graph of US merchandise trade deficits,

and have interpreted this coincidence as the evidence that US trade deficits

are driven by Yen/Dollar rates with the latter enjoying a two year lead

time. The theory of cyclical trade balance patterns, which says that the

trade balances are driven by the boom and busts of the economy, does not

apply here. If we assume that the trade deficits are driven by the economy

as the theory says, then we will be forced into a rather ridiculous conclusion

that the currency market participants are super smart and they, and only

they know what is going to happen to our economic fortune two years in

the future and adjust Yen/Dollar rate at present accordingly. We do not

accept this kind of eccentric argument, so we follow the interpretation

of Section 3 that it is today's Yen/Dollar rate that determines the US

trade deficit two year down the road. The next thing we want to know is

how the merchandise trade deficit is interacting with the economic growth.

With those understandings we will be able to say that Yen/Dollar rate drives

US merchandise trade deficit and in turn the ups and downs of merchandise

trade deficit determine booms and busts of US economy.

The correlation graph between

annualized

growth of real GDP of US and the ratio of

merchandise trade balance over current dollar

GDP, for 1982 to 1997, are presented in Fig. 4

with the data point for each year tagged by a

2 digit number, indicating the year. As we follow

the data points of "82", "83" and "84", it shows

an increasing trade deficits accompanied by

stronger growth in GDP, where the exploding

trade deficits were fueled by the strong Dollar vs.

Yen during the period of "a" to "b" in the

Yen/Dollar curve of Fig. 3. 1984, with a GDP

growth rate of 7.3%, had been the only year

since 1966 that US economic growth rate had

exceeded 6%, and apparently the growth was

over the natural growth potential of US like 4 to

5 % a year. Thus the growth rate fell back to

below 5% in 1985. However, the period of the

exploding trade deficit of 1982 to 1987 was not

over, so with the growth rate stuck near the

potential growth rate and with trade deficit

exploding, data points "85", "86" and "87" moved toward left along

a horizontal line labeled as "B" in Fig. 4. In the pre globalization era

studied in Section 2, transition from a phase represented by a slanting

line like "A" in Fig. 2 to another such an inclining line of another phase

was common, but never displayed any such horizontal multi-year line like

"B" in Fig. 4. We will call the horizontal line like "B", a "bridge". The

"bridge" of 1985 to 1987 apparently coincided with the first bubble of

corporate merger frenzy, and when the data points came to the end of the

bridge, the bubble burst. 1988 was the year that the data point retreated

to the bridgehead as US trade deficit shrank due to the reversal of the

trend of trade balance as shown in the bottom curve of Fig. 3, section

from "b" to "c". As US trade deficit retreated further and further as the

time advanced, data points of 1989, 1990, and 1991 had slide down along

the line "A", ending at slightly negative GDP growth rate of 1991. Another

push upward of US trade deficit, which started at 1992, push up the data

point of 1992 along the line "A". As the trade balance curve started to

stagnate in 1994 to 1997 (see section "d" to "e" of the trade balance curve

of Fig. 3), data points of those years are clustered together in Fig. 4.

Data points of 1991 to 2002 are

plotted

in Fig. 5, with years 1991 to 1997 and the

line "A" of Fig. 4 reproduced. The phase of

further exploding US trading deficit of the

section "e" to "f" in the trade balance curve of

Fig. 3, which was induced by the massive

currency market manipulation of Japanese

Government, produced the second "bridge",

labeled as line "D" in Fig. 5. This second bridge

was the period of the most recent bubble.

When it comes to the end of this second bridge,

the recent bubble burst. However, the down

turn of US trade deficit started in 2000 has

been rather shallow due to the China factor,

since China has become the major proxy

exporter whereas the currency of China is

pegged to US Dollar. Thus the data point

of 2001 has not been able to retrace the bridge

as in the case of 1988, but rather has formed

a new phase, labeled as line "C" in Fig. 5; we

are currently still in this most recent phase.

5. HOW IMPORTS AND EXPORTS ARE TABULATED IN GDP

Starting from this section, we

will turn our attention to theoretical backgrounds of the phenomena observed

in previous sections. In this section we will consider the way imports

and exports are handled in GDP tabulation, and show why the simplistic

explanation that trade surplus adds to and trade deficit subtracts away

from GDP is clearly in error.

Let us start by following the path

of an imported article, say a shirt. Let us assume that the price of the

imported shirt is $1 at the time when it passes through the custom. As

the shirt goes through various stages of retail channel, values are added,

and suppose it is finally sold to a consumer for $10. In the GDP report

there is a category called "final sales" or "personal consumption", and

this sale of the shirt, $10, will be added to the total amount of "final

sales". However, this tabulation is not correct, since GDP should only

calculate values produced domestically, and the first dollar of the shirt

is clearly not produced domestically; in other words GDP should have booked

$9 from the sale of the shirt, not $10 as done. That is the reason that

at the end, GDP creates an additional category called "imports" to subtract

this $1 from GDP; this "imports" is simply the total amount of imported

goods tabulated at the time when they pass the custom. The mistaken simplistic

view that imports subtract away from GDP comes from just looking at the

category of "imports" and think that more we import, more we subtract from

GDP. However, in the example of the imported shirt, if we have not imported

this shirt, we certainly will not subtract $1 from GDP due to the "imports",

but we also cannot book $10 from the sale of this shirt in the tabulation

of "final sales". Thus the net effect of not importing this shirt

is negative by $9 to GDP, not plus $1 to GDP as the simplistic explanation

trying to let us believe. After saying that it is also dangerous to think

naively that more we import, more positive GDP will become, since we must

weigh carefully the impact of the import on the domestic manufacturers;

the pros and cons of imports will be analyzed in the next section.

Now how about exports? The exports

are clearly values produced domestically and should be added to GDP. However,

in the major categories of GDP report, there is no place that is tracking

the contribution of exports. That is why there is another category called

"exports" in GDP, in which the total amount of exports as they pass through

the custom are tabulated and are added to GDP. It is also erroneous to

think that more exports means more plus to GDP, since we must weigh carefully

about what happens if the item is not exported but consumed domestically;

apparently the resources used to make exports will not be available to

make domestically consumable goods. The "imports" and the "exports" categories

in GDP are usually grouped together as "net export" though they have very

different characters in GDP tabulation as discussed above; the combination

into "net export" apparently causes further confusion and lead to the mistaken

simplistic thinking that trade surplus adds to and trade deficit subtracts

away from GDP. Usually the impacts of trades on GDP depend on the economic,

social and even psychological structures of a society and must be studied

case by case. In the following two sections we will derive some general

conditions under which imports and exports will boost or depress GDP.

From the discussion in this section it

should be clear that the simplistic explanation that trade surplus adds

to and trade deficit subtracts away from GDP is based on a misunderstanding

about how trade data are used in GDP tabulation. Another caution related

to this issue is in order. For example, on Aug. 14, 2003 US June trade

deficit is officially announced by the Commerce Department, and the trade

deficit turned out to be somewhat less than expected. Financial media immediately

reported that the estimate of the second quarter GDP growth will be adjusted

upward, thus giving an impression that positive trade balance is beneficially

to GDP and vice versa. What is happening here is that as discussed GDP

tabulation compute "final sale" and "imports" separately. The personal

spending data of June came out several weeks earlier than June trade data,

so economists has already used the actual data to compute "final sale"

of the second quarter, but the "imports" and "exports" categories for the

second quarter are only based on guess. When the real data has come out,

the guess about trade balances of the second quarter then need to be adjusted.

It does not mean that positive trade balance adds to GDP as the simplistic

explanation claims. Our study based on the actual data in previous sections

has already discredited such simplistic explanation completely.

6. IMPACTS OF MERCHANDISE IMPORTS

Our major concern here is that

strong Dollar induces explosive expansion of US trade deficit, and we want

to know how this explosive increase of trade deficit will influence the

growth of US economy. Thus we must analyze how imports and exports will

influence economic growth, not the other way around as done in the theory

of cyclical trade balance patterns. In this section we will consider the

impact of imports.

There are many varieties of imports.

Here we exclude the service imports. Service imports have vastly different

characteristics from merchandise imports. For example, the money spent

overseas by a domestic traveler is counted as service import, and the money

spent domestically by an oversea-visitor is counted as service export.

Such service exports are automatically counted in "the final sales" category

of GDP, so it does not need to be added to the "exports" category of GDP.

On the other hand, traveler based service imports do not contribute to

GDP, so it should not be added to the "net imports" category either. Other

kinds of service imports and exports, like the insurance bought from or

purchased by foreign companies, are directly added to "imports" and "exports"

categories. However, this kind of service imports and exports typically

does not have any multiplying power. For example, a service worth $1 purchased

by a foreign entity, is still only worth $1 if purchased instead by a domestic

company. Thus the effect of service trades on the economy is much less

prominent compared to the merchandise trades. Therefore, in this

article we will not consider the effects of service trades.

Within merchandise trades, the

monetary amount of imports can change either due to the change of

the quantity of imports, or due to the change of the import prices. The

quantity of imports of inelastic merchandises, like oil, does not change

very much even its price fluctuates widely. The effect on GDP due to the

change of oil price is quite obvious; if the price of oil jumps, it is

going to hurt GDP and vice versa. However, the amount of oil imports of

US (about 60 billion US Dollars a year, assuming oil price at $30 a barrel),

though is large, pales when compared to the overall merchandise trade deficit

of US, which is about 500 billion US Dollar a year. Thus in this section

we will only consider the merchandise trades excluding inelastic commodities

like oil.

To understand the effects of merchandise

imports, excluding oil, we first consider a virtual society where there

is no manufacturing activity at all as a pure example. All the economic

activities of this society is service oriented, like retail sales, financial,

real estates, insurance, health cares, and, of course, the activities to

import all the required manufactured goods from overseas. If a shirt, as

in the example given in Section 5, is imported, it literally adds nine

dollars to GDP since there is no domestic shirt making activity in this

virtual society so no worker will be laid off and no factory will close

its door due to this imported shirt.

The situation of this virtual society

can be looked at from a different angle. Suppose the central bank decides

to release more money into the society by either lowering the interest

rates or by reducing the reserve requirements of the commercial banks,

whereas the total quantities of imported goods are fixed, then due to the

rule of supply (fixed amount of goods) and demand (more money), only thing

will happen to the society is inflation. Thus the nominal GDP will increase,

but the inflation adjusted real GDP will remain exactly the same no matter

how much extra money the central bank injects into the society. In order

for the real GDP to grow, the quantities of imports must also grow. Therefore,

in this virtual society, more imports means more growth in the real GDP.

In that sense we may call this virtual society "the heaven of merchandise

imports".

If the currency of this virtual society is left to the free currency

market, it will lose value quickly and the virtual society will be forced

to have manufacturing sectors since it can not afford to continue to import

large quantities of goods. Only way that the virtual society can sustain

its pure form is for the governments of other societies to artificially

buy the currency of that virtual society to support its value, just as

Japanese Government is buying US Dollar.

In a real society, there may exist

some manufacturing sectors that are exposed to the competition of imported

goods. Let us assume that the shirt making business is within such a manufacturing

sector. When a $1 shirt, as discussed in the previous section, is imported,

a domestically manufactured shirt sold, say for $1.5 by the manufacturer,

is pushed out of the market. If the capital and labor used to manufacture

the domestic shirt cannot be redeployed to other sector, then GDP will

lose this $1.5, assuming that the domestic shirt will also generate $9

if it goes through the retail channel. If the capital and labor can be

redeployed to some other sector, GDP will most likely gain since this newly

produced value will open up a new retail channel and will generate a large

sum of its own added values that is surely more than $1.5. However, if

the imported shirt does not compete with any domestic shirt, than the imported

shirt will add $9 to GDP, just like the case in the virtual society. Thus

whether imports will be beneficial to a society or not depends on how much

new opportunities exist, and how close the society is to the virtual society

without any manufacturing base.

7. IMPACTS OF MERCHANDISE EXPORTS

Some societies are gifted by nature

in some special ways, like many Middle East Countries are abundant in oil,

and US is very favorable for mass-producing agricultural goods. For those

countries, small input will yield large outputs of those naturally favored

goods. Also it is difficult for other places to replace those naturally

bestowed goods. Here we are not going to consider the export of this kind

of natural resources, but concentrate on the general merchandises that

are highly replaceable depending on the cost of production in a specific

region. We also limit our consideration of the impact of general merchandise

export on a matured, or developed economic entity; the analysis of the

impact of exports on a less matured economy, or developing country exposes

various unique, intriguing and interesting questions, and deserve to be

studied in a separate article of its own.

Let us consider a matured economic

entity growing at its maximum potential, so that its capital and labor

are fully deployed. Suppose there is a production of a shirt, and it is

valued at $1 when it leaves the factory and is sold to a consumer for $10

after going through various stages of retail channel. Thus this shirt contributes

$10 to GDP. Now suppose by some artificial intervention (like government

action) this shirt is taken out of the domestic circulation and is exported.

GDP tabulation will add $1 to the "exports" category, but the "final sales"

account will lose $10. The net effect of exporting this shirt is thus negative

by $9 to GDP. Due to this export, the capital and labor in the retail

channel to generate $9 value if the shirt had been sold domestically is

now idled. In an ideal situation, this idled capital and labor can be redeployed

to some other sector instantaneously to reproduce the lost $9. However,

even in this ideal situation the best GDP can do is to become the same

as before the export of the shirt. In real case there is always a time

delay in recouping the lost $9 due to the export, so GDP almost always

lose. This is intuitively easy to understand since when an economic entity

is growing at its maximum potential, there is simply not possible to accelerate

its GDP further without fixing its structural problems. It also points

out the impossibility to boost GDP by artificially increasing exports in

a matured economic entity under normal conditions, in total contradiction

to the simplistic explanation. Artificially increasing exports will rather

cause GDP to shrink for a matured economic entity when it is growing near

its natural potential. This is why Japan has sunk into a prolonged recession

as its government has deliberately destroyed the value of Yen in order

to make its trade surplus explode.

Only when the matured economic

entity is already in a deep recession or in a depression and there are

plenty of idled capital and labor, then by some artificial means to deploy

those idled capital and labor for producing exportable goods will help

GDP, like the case from 1946 to 1947 in US discussed in Section 2. However,

any artificial action to increase export, even under those miserable conditions,

will usually have severe side effects and the harm to its economy will

out weigh the benefit from the increased export. If a matured economic

entity is in trouble, it is better to stimulate its domestic consumption

rather than to take artificial means, like deliberately destroy the value

of its own currency in order to increase its exports.

8. YEN/DOLLAR TIME DELAY, AND BOOM BUST AND THE BRIDGE

In Section 3 we have observed that

major trend changes in Yen/Dollar exchange rate is translated into significant

shifts in the pattern of trade deficit with a time delay approximately

two years. It may be surprising to some that the change in currency exchange

rate takes so long to influence the trade balance. To answer this question,

let us consider two countries A and B, and assume that both countries have

factories to manufacture shirts for their domestic markets respectively,

and also let us assume that at the beginning the costs of manufacturing

shirts in A and in B are similar. Suppose the currency of A suddenly move

up sharply against the currency of B so that the cost to make a shirt in

A becomes substantially higher than the cost in B. The shirt company in

B will naturally take advantage of the situation by expanding its shirt

making capacity, make more shirts, export them to A, and drive the shirt

company of A out of business. In order to do this the shirt company in

B must draw up a plan, get the financing for the plan, physically expand

the shirt manufacturing facility, make more shirts, and then export to

A. All those steps take time and thus there will be a long time delay from

the currency movement to the actual trading of a shirt between A and B.

It happens to be that this unavoidable time delay is about two years in

the real world.

In Section 4 when we studied the

"bridge" phenomena, we said that those bridges correspond to bubbles. Besides

the empirical facts that the physical timing of a bridge coincides with

the era of a bubble, there are also theoretical reasons why a bridge should

be related to a bubble. As discussed in Section 6, imports will boost the

economic growth if the capital and labor displaced by the imports can be

redeployed to other fields quickly. When imports flow in too rapidly,

the ability to redeploy labor and capital will be strained and the growth

rate of GDP will hit a ceiling, whereas the ratio of merchandise trade

deficit over current dollar GDP will expand rapidly. Thus a bridge is formed

in the correlation graph like Fig. 4 and 5. In case of the Reagan era boom

and bust, the retreat of US merchandise trade deficit, starting near the

end of 1987, was significant, so the ratio of trade deficit to GDP move

rapidly toward right, and the economy settled back to the phase where the

bridge had sprung. In the boom of Clinton era the retreat of US merchandise

trade deficit, starting at 2000, is measured since the fall of Dollar vs.

Yen in 1998 to 1999, though was sharp, but was not really drastic. Thus

the US economy has not be able to return to phase "A" of Fig. 5 but has

entered into a new phase "C" in Fig. 5, which encompass a much higher ratio

of trade deficit to GDP than the previous phase of "A" in Fig. 5.

It is interesting to observe that

if a society is near the virtual society without any manufacturing base,

the "bridge" phenomenon will not appear, since in the virtual society,

more import simply means more growth assuming that the retail sector is

very elastic. Thus the data points on a correlation graph simply move toward

the upper left direction along a slanting trend line like the line "C"

in Fig. 5 if trade deficit increases. In that sense the appearance of bridges

in both the Reagan year bubble and the Clinton year bubble means that US

is still not yet near the virtual society with most of the manufacturing

sectors extinguished.

Now about the reason why a stock

market bubble often accompanies "bridge" phenomena. When US runs a merchandise

trade deficit, US Dollar is handed over to foreigners. The foreigners may

sell the dollar to other foreigners, but the net amount of the dollar will

remain in the hands of foreigners; in recent days those dollars will be

most likely ended up in the hands of foreign governments. Since US Dollar

is not legal tender in the countries with large trade surpluses, those

foreign owned dollar must be deposited back to US. The foreign dollars

in US will not buy consumers goods, but will be invested, for example,

in US treasuries. When those foreign dollars buy US treasuries, some US

investors, most likely some institutions, must sell the treasury securities

to those foreigners. The proceeds of the sale of treasury securities received

by domestic institutions then will be invested in other fields, and stock

market will benefit directly. When the merchandise trade deficit starts

to shrink, less money comes into stock market from this rout. That is why

in a period of explosive rise of merchandise trade deficit, a stock market

bubble will appear. At the time when the trade deficit starts to shrink,

less money of this trade deficit rout will come into the stock market,

and the bubble will start to burst. This kind of stock market bubble burst

cycle had appeared in Reagan era that ended in 1987, and again in Clinton

era and the bubble burst in 2000.

9. THE FUTURE OF US ECONOMY

Through out this article, we have

repeatedly advanced the claim that strong Dollar induces large merchandise

trade deficits, and the large trade deficit in turn boosts US economy and

creates bubbles. It has always been the declining trade deficits that burst

bubbles and introduce economic down turns. Some may get an impression that

strong Dollar and the delayed explosion of merchandise trade deficit, even

it is artificially introduced by the action of Japanese Government, is

our friend, and weak Dollar induced by the currency market to discourage

the huge trade imbalance, and the subsequent shrinkage of merchandise trade

deficit is our enemy. However, it is not the case. To use merchandise trade

deficit to boost economy is like to take illicit drugs to achieve temporary

stimulus; eventually it will destroy the whole economy and will reduce

an economic superpower into a second rate economic back water. Let us see

the reason of this conclusion.

From very early in the history

of humanity the accumulation of monetary commodities, like gold and silver,

is considered to be the measure of wealth. This measure applies to individuals

and also to governments. At the time when gold is used to settle trades,

if a country, which does not produce significant amount of gold, wants

to accumulate more gold, it needs to run a trade surplus. The thinking

that the goal of the economic policy of a country is to let it accumulate

more gold, or to run the maximum possible trade surplus is called "mercantilism".

Before the great depression mercantilism was the prevailing economic wisdom

of the world. After the great depression mercantilism has given way to

modern economics. Modern economics tries to evaluate the richness of a

country not based on how much gold it owns, but on the living standard

of the people of the country. However, the living standard of the people

is not easy to quantify. In the modern times when the quantification is

touted as the ultimate goal for economics to attain the similar respectability

as natural sciences, the concept of the living standard of the people is

replaced by an objective measure like GDP and its growth. In this article

we have shown that the growth of real GDP of an economic entity, and the

trade balance is mostly anti correlated, thus trade deficit is desirable

if our only goal is to achieve high growth rates of GDP. However, GDP is

only a view from one direction of the condition of an economic entity.

If we concentrate only on GDP, we are prone to fall into a folly that is

frequently uttered on many financial media: Suppose a natural disaster

befalls on Country A and destroys a large number of houses. This loss of

property will not be reflected on GDP of A, whereas the subsequent effort

to rebuild the lost houses will be recorded as big gains for GDP. Thus

many financial commentators will say something like, "The disaster is a

human tragedy, but it is a big plus for the economy." The error that those

commentators have committed is to ignore the other equally important indicator,

the "national account balance". The "national account balance" is computed

as follows: Sum the values of all assets physically based in Country A.

Add all the claims that the government, corporations and individuals of

Country A have against foreign sources, and finally subtract all the claims

that any foreign source has against the entities of Country A. The last

two terms combined together is called the "net external asset" that can

be positive or negative. Positive net external asset adds to the national

account balance, and negative net external asset subtracts away from the

national account balance. The negative net external asset is also called

the "net external debt". The national account balance is the measure to

gauge the net worth of Country A. If the national account balance dips

down to zero or negative, it is equivalent to a familiar financial condition

of individuals called "bankruptcy". When a natural disaster hits and many

houses are destroyed, it is the national account balance get reduced and

the living standard of the people of Country A is reduced; apparently it

is a highly undesirable condition for Country A. The rapid growth of GDP

in the frenzy of rebuilding only reflects the efforts to rebuild the national

account balance back to the pre disaster level. Therefore, it is purely

against common sense and against the logic of modern economics as well

to call such natural disasters as plus to the economy of Country A.

Quite a few countries in Latin

America, Asia and other places have experienced currency crises after running

significant trade deficits for some time. Those currency crises have occurred

because those countries must settle their trades with other countries in

dominant currencies, like US Dollar. When the foreign currency reserve

of the country is exhausted, its import will plummet, causing GDP to fall

sharply as discussed previously in this article. Hot money that has entered

the country under the misjudgment of its money managers will panic and

want to escape from the country. If the currency of that country is floated,

then the currency will fall drastically to cause further panic and so on

and so on until its economy collapses and requires the aid of outside entities,

like IMF. At the time of the currency crises the national account balance

of that country is usually still in black. Then how about a country like

US whose currency is widely accepted as the settlement currency of international

trades? There is no rule that US Dollar should be accepted as an international

trade settlement currency. Foreign parties accept US Dollar as the payment

for their goods only based on the historical trust built toward the Dollar.

If their confidence wanes, US Dollar will lose its value against other

currencies in the currency market. Studying the constant tug of war and

the cat and mouse type engagement between the currency market and Japanese

Government, it is fair to say that the trust of foreign private parties

toward US Dollar has waned a long time ago due to the run away US trade

deficit. It is purely due to the enormous market manipulation to destroy

the value of Yen and to support US Dollar undertaken by Japanese Government,

foreign private parties are still accepting US Dollar as the payment for

their goods since they know that they can always sell their US Dollar to

Japanese Government for other currencies.

Now let us project what will happen

in 20 years if the current condition persists. To estimate what is going

to happen in the future for US economy, we need first to understand what

is the net external debt of US at present. US net external asset turned

to zero at 1985. By adding up all the current account deficits since 1985

we will get a reliable picture of what the net external debt is at present.

At the end of 2002 it is like 3.2 trillion dollars. The net external debt

probably will grow like 550 billion dollars in 2003. Assuming that Japanese

Government, with the help from China, will support the value of Dollar

to the level that US can run a merchandise trade deficit of about 5% of

GDP, near the line "C" in Fig. 5, for a long time to come. Also let us

assume that US current dollar GDP will grow like 4.0% a year (e.g. 1.5%

inflation and 2.5% real growth), and that US service trade surplus will grow

such that the burden of financing the external debt will cancel out with

the increasing service trade surplus. Under those conditions it is possible

to estimate that at 2023 US external debt will be 18 trillion dollars and

the current dollar GDP will be about 22 trillion dollars. Further assuming

that the total value of US based assets is similar to the current dollar

GDP, then at 2023 the national account balance of US will be 22 - 18 = 4

trillion dollars. At the end of 2003, US national account balance will

be about 10.5 - 3.75 = 6.75 trillion dollars. Thus in 20 years US national

account balance will shrink by 2.75 trillion dollars, but nominal GDP, or

the consumable sums, will jump 220%, and inflation adjusted real GDP will

grow by 164%. The merchandise trade deficit will be 1.1 trillion dollars

a year. On the other side of the ledger, we need to consider what is going

to happen to Japan. Currently Japan's current dollar GDP is about

5.0 trillion dollars, and the external asset is around 1 trillion dollars

in black. This means that the national account balance of Japan is

about 6 trillion dollars. The growth of Japan's current dollar GDP is slightly

negative; if we assume deflation is 2% and the real GDP growth is 0%, then

the current dollar GDP is shrinking 2% a year in Japan. Since Japanese

trade surplus must increase to accommodate strongly expanding US trade

deficit, the ratio of Japan's trade surplus to its GDP will increase and

the growth of real GDP will slump further as we have discussed throughout

this article. Even if we are very optimistic and only assign a 3% shrinkage

a year in the current dollar GDP of Japan, the current dollar GDP of Japan

at 2023 will be like 2.7 trillion dollars. Suppose Japan holds 50% of 18

trillion dollar of US external debt, then Japan's national account balance

will be 2.7 + 9.0 = 11.7 trillion dollars at 2023, a substantial expansion

from the present level of 6 trillion dollars.

Let us translate those numbers into plain

language. The condition at 2023 will be as follows: American net worth

will shrink substantially by 2023, but an average American citizen will

live in an estate home built with money borrowed from Japan, will

drive Japanese made luxury automobiles purchased with the money borrowed

from Japan, and will dine daily in high class restaurants and charge the

expense on credit cards which are again financed with the money borrowed

from Japan. At that time US will become a virtual society, as discussed

in Section 5, without any manufacturing base. US Federal Reserve System

will become the agent of Japan, China, Taiwan, Hong Kong, and Singapore

who collectively hold 18 trillion dollar worth of claims on US. On the

other side of the Pacific, Japan will become the richest nation on

earth according to its national account balance, but an average Japanese

will be peddling bicycles instead of driving automobiles, a Japanese family

will be clamped into a 300 square feet apartment, and an average meal of

Japanese citizen will return to a box of white rice with a red preserved

plum sitting in the middle of the box, a typical diet of Japanese during

the World War II. Japanese Government will be more occupied in managing

9.0 trillion US dollar located in US than to be bothered with running a

meager 2.7 trillion Dollar Japanese domestic economy. If we think such

a picture is too ridiculous to be true, then we must conclude that US Dollar

will suffer a catastrophic collapse, the runaway US trade deficit will

be curbed, and US economy will sink into a depression on the way to 2023.

REFERENCES

1. US economic data used in this article are published by US Commerce

Department

and US Federal Reserve System.

2. Chih Kwan Chen, "Economic Crises of Japan, Asia and Beyond", (1998).

3. G. Corsetti, P. Pesenti, and N. Roubini, "What caused the Asian currency

and financial crises?

Part 1: A macroeconomic overview" (1998).

Return to the Home Page of the Website