Review & Forecast 1: THE RISE AND THE SELF-DESTRUCTION OF THE GLOBALIZATION SCHEME

SECTION 8. CURRENCY MANIPULATION AND THE DOT-COM BUBLE:

The role of Japan's near-zero interest rate policy

by

Chih Kwan Chen

forcastglobaleconomy.com

(July 17, 2014)

Prelude

Reaganĺs junk-bond-bubble took four long years to unwind. During the first phase of the runaway

U. S. trade deficit in Reagan era, the trade deficits with Japan dominated the scene. In early

1985, major industrial nations reached an agreement to bring down the exchange rate of U. S.

Dollar vs. Japanese Yen to reduce the U. S. trade deficit with Japan. Thus Dollar tumbled down

quickly from $1.00 = 220 Yen level to around $1.00 = 125 Yen. With the usual 2 to 3 year delay

for a major trend change in the exchange rate to be reflected on the actual trade balance1,

the runaway U. S. trade deficit reached the peak by late 1987. Seeing no more increase

in the financing of the junk-bond-bubble through U. S. trade deficit, institutional investors

switched on the newly fashionable trading software of ôdynamic hedgingö. The result was

the rush to the exit door at once by big boys in the market, triggering the infamous 1987 stock

market crash.

At the same conference of major industrial nations at early 1985 when the devaluation of Dollar vs.

Japanese Yen was agreed upon, Japan had promised to stimulate its domestic economy to divert

more of its products away from exports and into domestic consumption. At the same time Japan will

increase its imports. By the time of 1987 stock market crash, Japanese economy boomed into a bubble.

With the help of sharply devalued Dollar and increased demand from Japan, U. S. manufacturers

rebounded and carried the U. S. economic growth throw 1988 and 1989.

Junk bonds issued in Reagan era matured typically in 5 years. At the time of 1987 stock market

crash, most of the junk bonds were still 4 years away from the maturity. This meant that those

companies funded by the junk bonds could have operated another 4 years in spite of the stock market

crash. On the trade deficit front, from the end of 1987 U. S. trade deficit kept falling

to a very low level by 1991. When a large number of junk bonds must be refinanced in 1991,

the financing was not available due to vastly shrunk U. S. trade deficit. Massive default

and bankruptcy of those junk financed entities followed, triggering the 1991 recession. Across

the Pacific Ocean, by 1990 Japanese Government had started to rein in the overstimulated bubble.

The 1991 recession forced many businesses to undergo massive restructuring. In order to cut costs

many experienced workers were laid off, replaced by inexperienced young workers. A

fashionable phrase of that time was, ôthe career of a computer scientist ends at age 40.ö

This kind of folly, of course, cut into the strength of the U. S. industrial might. It was the

first sign how the evil scheme to hook the U. S. on to the runaway trade deficits is destroying

an industrial giant. In this section, we will see how the suicide of an industrial giant evolves

further. In the next section we will witness the final phase of this suicide under the beautiful

name of ôglobalizationö.

A short taste of the power of a free currency market

The painful restructuring during the 1991 recession had left many U. S. businesses lean and could

move quickly once the recovery started in 1992, though such advantage was achieved by cutting off

own muscles, bones and brains essential to the long term healthy growth. As the U. S. had emerged

from the recession, consumer demands rose, and the trade deficit with Japan had started to expand

again. From 1992 to 1995 there were no noticeable manipulation of Yen-Dollar exchange rate in the

currency market by governments, so the vigilante mechanism of the free currency market to prevent

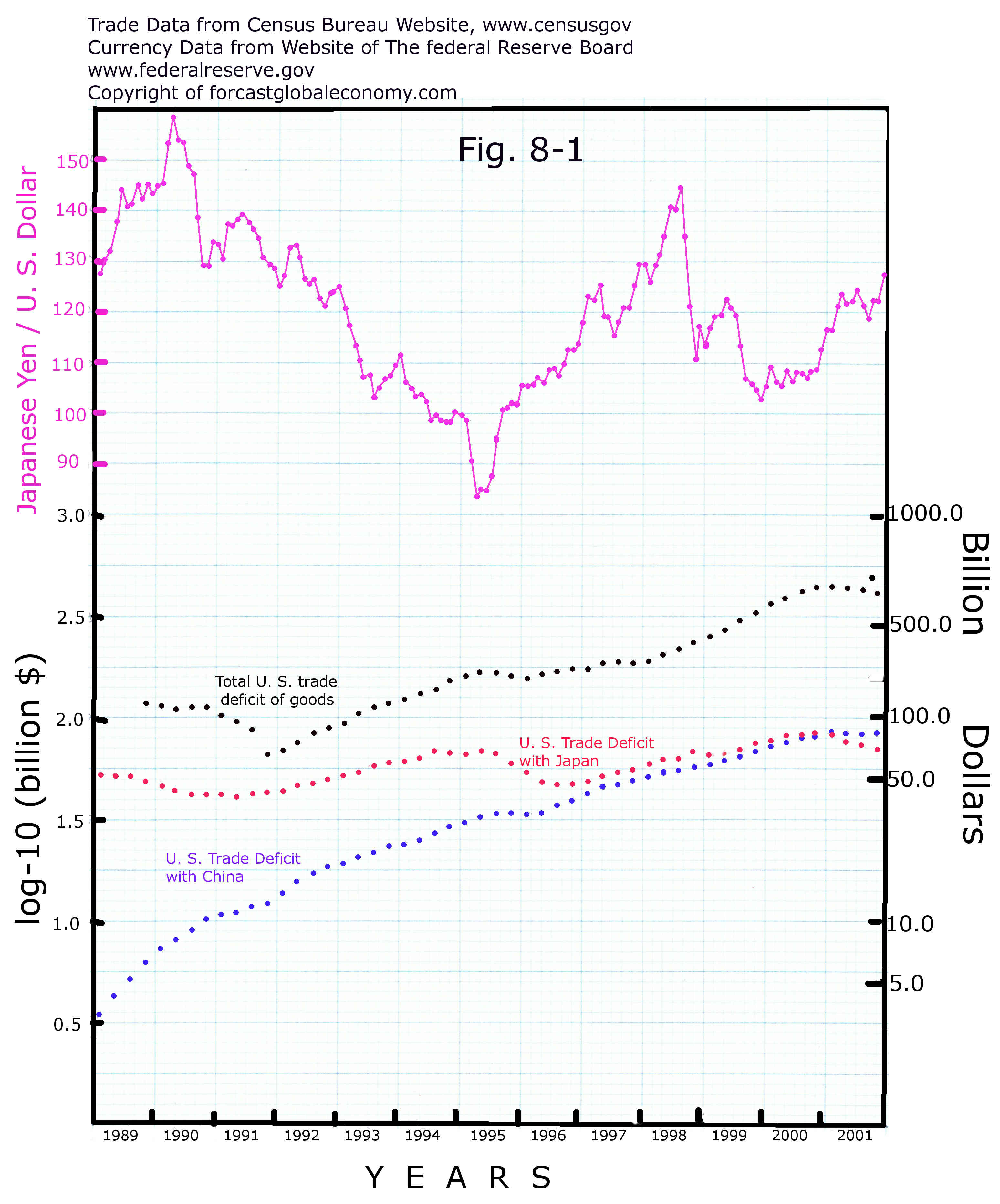

the run away trade imbalance worked. Let us follow the data shown in Fig. 8-1 at the right to trace

how this vigilante mechanism was in action.

The painful restructuring during the 1991 recession had left many U. S. businesses lean and could

move quickly once the recovery started in 1992, though such advantage was achieved by cutting off

own muscles, bones and brains essential to the long term healthy growth. As the U. S. had emerged

from the recession, consumer demands rose, and the trade deficit with Japan had started to expand

again. From 1992 to 1995 there were no noticeable manipulation of Yen-Dollar exchange rate in the

currency market by governments, so the vigilante mechanism of the free currency market to prevent

the run away trade imbalance worked. Let us follow the data shown in Fig. 8-1 at the right to trace

how this vigilante mechanism was in action.

In Fig. 8-1 the purple line is for the Yen/Dollar exchange rate plotted in monthly intervals. The black

dots are 12 month moving sum of total U. S. merchandise trade deficit in quarterly intervals. The red

dots are 12 month moving sum of U. S. merchandise trade deficit with Japan, also in quarterly

intervals. It is worth to point out that 12 month moving sum should be read as 6 month delayed

statistics. For example, the red U. S. merchandise trade deficit with Japan had started to form a

broad bottom from the fourth quarter of 1990, but the actual situation is that the bottom had started

to form from the end of the second quarter of 1990 since the moving sum of the fourth quarter of

1990 is the sum of the first quarter to the fourth quarter of 1990 with the center at the boundary

between the second and the third quarters.

The massive devaluation of U. S. Dollar against Japanese Yen started in early 1985 and continued

until 1987. Since a significant trend change in exchange rates takes two to three years to be

reflected on the actual trade balance1, the U. S. trade deficit with Japan peaked in

1987 and declined until early 1990. Matching with the declining trade deficit with Japan, the

free currency market pushed up the value of Dollar vs. Yen, creating the peak in the purple Yen/$

curve in Fig. 8-1 at early 1990. As the effect of the massive Dollar decline of 1985 to 1987

dissipated by early 1990, U. S. trade deficit with Japan turned to sideways, and then started to

rise as the U. S. economy started to recover from the recession. Seeing this sea change, the free

currency market started to push U. S. Dollar lower vs. Japanese Yen in order to curb the rising

U. S. trade deficit with Japan. This effort to push down U. S. Dollar to curb U. S. trade deficit

is shown in the steep drop of the purple curve in Fig. 8-1 from 1990. However, at that time

period, Japan's mighty bubble of late 1980s had burst already, directing Japanese industries to

turn their attention to export again. Japan was still in the stage of vibrant innovation and

productivity gain so the expanding U. S. trade deficit with Japan was not easy to slow down.

It took fully three years for the massive devaluation of Dollar vs. Yen to make the trade

deficit to flatten out in 1993, and another two years, in early 1995 for the deficit to decline;

by that time Dollar had been devalued to 80 Yen/Dollar already. As the trade deficit with

Japan rounding down, U. S. economic expansion had also slowed down, causing panic to both Clinton

Administration and Japanese Government. Thus the stage was set to the following era of disastrous

monetary policy.

Currency Manipulation of the Second Kind: Japan's near zero interest rate policy

Japan is poor of natural resources. She must export manufactured goods to get the hard

currency to cover the cost of importing raw materials. During 1950s and 1960s, any time when her

economy boomed, the robust domestic consumption caused increased imports and the trade deficit so

the economy needed to be slowed down and a recession followed. Gradually people of Japan developed

the merchatilism-like tendency to treasure trade surplus, larger the better. After the burst of

Japan's gigantic bubble at the turn of 1980s to 1990s, Japanese industries turned their attention

to exports again and were rejoiced as the trade surplus started to rise. Then as described in the

previous subsection, the vigilante mechanism of the free currency market set in, pushing Japanese

Yen steadily higher, eventually to 80 Yen/Dollar from the level of 125 Yen/Dollar, in order to rein in the

Japan's expanding trade surplus against the U. S.. Japanese Government must have disappointed to

see the free currency market had dashed her hope to use trade surplus to reinvigorate Japanese

economy so decided to use near-zero interest rate policy to achieve her goal. The scheme works

as follows: Near-zero interest rate will induce international speculators to engage

in yen-carry trades. A yen-carry trade is for a speculator to borrow Yen at near-zero

interest rate, sell the borrowed Yen for Dollar, and invest the dollar proceeds in high

yielding Dollar denominated instruments. It is at the process of selling borrowed Yen

for Dollar that pushes Yen down vs. Dollar. This scheme was apparently approved by the Clinton

Administration, since when Japan's near-zero interest rate policy was put into action at the middle

of 1995 and Dollar flew higher vs. Yen as the purple curve in Fig. 8-1 shows, Clinton Administration

immediately came out with the slogan of "Strong Dollar Policy" to praise the rapidly climbing Dollar.

To use near-zero interest rate to devaluate a currency, like Japan did in 1995, is a kind of

blatant currency market manipulation that we call "The Currency Market Manipulation of the Second Kind".

Around 1995 Japanese manufacturing capacity was not fully utilized due to the lingering effect of the

burst of the late 1980s' bubble and the strong Yen that curbed the exports. When the near-zero interest

rate policy was introduced and Yen started to drop sharply vs. Dollar, those idled manufacturing

capacity was quickly thrown back into churning out exportable goods. Thus Japan's declining trade surplus

against the U. S. was arrested in 1996 and started to turn up again. Along with the climbing U. S. trade

deficit with Japan, so was the overall U. S. merchandise trade deficit since many developing countries

were surrogate exporters of Japan in the low cost-low technology products. The sharply elevated trade

deficit then stimulated the Clinton Dot-com bubble2.

Asian Financial Crises, the trigger of bursting Clinton Dot-com Bubble

Japan's near-zero interest rate policy has generated severe consequences both in the domestic

front and in the international front instead of pushing Japan's economic prosperity through

the devaluation of Yen and increased trade surplus. On the domestic front, the policy has

trapped Japan into the prolonged economic stagnation3. At the time of 1995 when

the near-zero interest rate policy was introduced, Japanese worker's average retirement age

was about 55 and Japan's social security system was far from adequate to support such a young-age

retirement. Average citizens of Japan need to save a substantial portion of income as retirement

nest eggs. Since the retirement saving depends heavily on the interest compounding, near-zero

interest rate policy cut down the retirement saving substantially. The response of Japanese workers

to the unexpected adverse effect on the build-up of retirement nest eggs was to cut back their

consumption and to save more. The chain reaction of more saving, less consumption, shrinking

business sales, pressure on wages and salaries, more saving and so on, has pushed Japan into a

self generated trap of the great stagnation.

The favorite vehicle for retirement saving in Japan was 3 to 5 years saving certificates issued by

government sponsored post offices and private banks. At the beginning of the near-zero interest rate policy

the pain to the private saving was not immediately felt. The near-zero interest rate policy naturally

meant more money creation to stimulate the economy. Thus for a short while the stimulant plus the

increased exports seemed to have lifted Japanese economy, but soon the bad impact of the near-zero

interest rate policy on the international front boomeranged to hit Japan at the time of above

mentioned domestic chain reaction took place to force Japan into the stagnation for more than 15 years.

The international chain reaction started from The Asian Financial Crises as will be discussed below.

As Japan becomes the power house of manufacturing consumer goods, the average wage in Japan rose

rapidly to make the manufacturing of labor intensive products not economical within Japan.

Starting from 1960s, more and more Japanese manufacturers have tried to outsource labor

intensive productions to low labor cost developing countries around Asia. Before

the globalization of 1980s, the existing tariff barriers limited the scope of such

outsourcing. The first target of Japanese outsourcing was Taiwan. As a former colony

of Japan, but not like Korea, many in Taiwan are friendly to Japanese. Under the strong authoritarian

control there were neither labor disputes nor environmental movements in Taiwan at that time.

Those conditions attracted many Japanese manufacturers to Taiwan. Idled labor resource in Taiwan was

utilized and Taiwan steadily climbed the economic ladder. We call such a development model

"Taiwan Model4". Once the era of globalization dawned in 1980s, the Taiwan Model really

shined; the consumer market in the U. S. was flooded by "made in Taiwan" inexpensive consumer goods.

By the latter half of 1980s, the average wage in Taiwan had also increased quite a lot, and the general

public of Taiwan has started to pay more attention to the environmental pollution by industries. However,

under the strong authoritarian regime of Chang Ching-kuo, the son of General Chang Kai-shek, that

regarded Communist China as the arch enemy, not many Taiwan merchants dared to relocate into China,

so some of them had outsourced their factories to other Southeast Asian countries. Also Japanese

manufacturers have started to outsource their factories to various Southeast Asian countries

instead of Taiwan. Naturally "Taiwan Model" is widely copied in those places, too.

In Eastern Asia, South Korea has not strictly copied "Taiwan Model". As a former colony

of Japan Korean dislikes Japanese and direct investments from Japan are not welcomed. Instead South Korea

borrowed heavily from Japanese banks to buy the technology and manufactured the inexpensive consumer

goods by herself. Thus all the East and Southeast Asian countries followed "Taiwan Model" one way or

the other, and they have advanced economically based on Japanese outsourcing of labor intensive

manufacturing. They exported their products mainly to the U. S. and improved their balance of

payments until 1995.

No matter the strict "Taiwan Model" or its variation like adopted by South Korea, one tactic used

by all is to peg their currencies to U. S. Dollar. To peg a local currency to Dollar, the local

goverment needs to intervene the currency market constantly to keep the exchange rate of the local

currency to Dollar stable. Such operations are a kind of blatant currency market manipulation.

Since the designers of the globalization scheme and the eager promoters of the scheme, that is,

successive U. S. Administrations, never tried to outlaw currency market manipulations, the tactic of

"pegging to Dollar" was also overlooked. The motivation of the U. S. not to outlaw currency market

manipulation is discussed in length in Sections 1 to 6 of this review article2.

The tactic of "pegging to Dollar" and more aggressive blatant manipulation of currencies

have been used widely until today.

As a country evolve along Taiwan Model and climbs up the economic ladder, it will start to run trade

surpluses. Its exporters will receive dollars for their exports and need to sell the dollars for the

domestic currency to pay for their next batch of productions. Its importers need to buy dollars

by selling the domestic currency to purchase foreign goods. Running trade surplus means that there are

more dollars for sale than the demand for dollars. Under a free currency market without any

manipulation, the value of the local currency will go up against Dollar, the cost of production

will rise, and the trade surplus will shrink. This is called the vigilante mechanism of the free

currency market to prevent the runaway trade imbalance and thus keep the global economy away from

the crash. However, the countries embracing "Taiwan Model" naturally do not want to see their string

of trade surplus be cut short by the vigilante mechanism of the free currency market. The government

will enter the currency market to buy up the surplus dollars with the domestic currency to nullify

the vigilante mechanism of the free currency market and keep the domestic currency pegged to Dollar.

The domestic currency used to purchase unwanted dollars, of course, is created by the central bank.

As the trade surplus increases, more domestic currency is created and the domestic economy will be

stimulated to generate bubbles. The real estate bubble is usually the easiest one to pop up. As bubbles

lift their uglyheads, the greed of getting richer prompts people to borrow more money to gain more

from the bubbles. On the other hand international capitals that anticipate that the "Dollar Pegged"

host currency will eventually be forced to appreciate vs. Dollar, and are eager to lend to the ones

wanting to borrow in order to establish a foot hole to share the fruit of the bubbles.

By 1995 many small Asian economies were in such a bubbling state. However, such unstable

bubbling state is very easy to be toppled by an external shock; in this case the external

shock was Japan's near-zero interest policy that induced the "Asian Financial Crises".

As has been pointed out in the preceding subsection, Japan's near-zero interest rate policy had

unleashed a flood of "Yen carry trades" and boosted the value of U. S. Dollar sharply higher vs.

Japanese Yen. Since the currencies of small Asian countries following "Taiwan Model" are pegged

to U. S. Dollar, the currencies of those Asian countries also appreciated sharply against

Japanese Yen, causing Japanese manufacturers to lose incentive to further outsource their labor

intensive operations to those small Asian economies. The trade surpluses of those countries diminished

and then turned into trade deficits. The demand of dollars from the importers overwhelmed the supply

of dollars from the exporters. The free currency market started to push down the value of the

currencies of those small Asian economies. Those Asian governments had no choice but to step into the

currency market to buy up their unwanted domestic currencies, using the Dollar reserve accumulated

during trade surplus days, otherwise the international capitals would have escaped in drove and the

whole economy of those countries collapsed. However, Japan's near-zero interest rate policy with the

full endorsement of Clinton Administration persisted, and those small Asian economies soon exhausted

their Dollar reserve and collapsed anyway. The first one went down the drain in July, 1997 was

Thailand. The collapse of Thailand naturally induced the international capitals to try to exit from

other economies in the similar state, and triggered the chain reaction of collapses. The one hit

Japanese banks the hardest, of course, was the collapse of South Korea that had generated a large

scale banking crises in Japan. Japanese banks cut back loans to small businesses to reduce leverage

to save themselves. Many small businesses in Japan failed, further reducing the consumer spending.

Under such a condition Japanese monetary authority has been painted into a corner created by

itself, not dare to raise interest rate and forced to do quantitative easing after quantitative

easing to prolong the near-zero interest rate policy. Thus Japan has entered into the endless

stagnation3 that we call as "Japan Syndrome".

After the Asian Financial Crises, IMF stepped in and tried to stabilize the currencies of fallen

Asian angels with $30 billion injection, but under the condition that those Asian countries rein in

government spending and install higher interest rate to help to bring back international capital and

to stabilize their own currency. The high interest rate policy put many entities out of business,

but had indeed stabilized the currencies. Those fallen angels gradually regained the growth

potential. The contagion of such a calamity certainly will not be limited to Asia alone.

Russian at that time was the competitor of those Asian economic entities for the

manufacturing of inexpensive consumer goods. With sharply devalued Asian currencies,

Russia certainly could not have maintained its currency peg to Dollar. In the first half

of 1998, Russian currency collapsed, resulting in the Russia default. A large hedge fund

sized around $100 billion was caught holding a lot of Russian debt and was near

insolvency. From the fear that the failure of that large hedge fund, "Long Term Capital", will shake

the whole financial structure, then FED Chairman Greenspan called in Wall Street big shots and pressed

them to jointly bail out Long Term Capital. At that juncture, Clinton Administration realized the

poisonous nature of its "Strong Dollar Policy". In the summer of 1998 U. S. and Japanese

Governments jointly intervened in the currency market to bring down the high flying U. S. Dollar.

As the result Dollar fell quickly from the level of 170 Yen/Dollar to the level of 125 Yen/Dollar.

By the middle of 1999 the contagion spread further to Latin America, and Dollar fell further to

110 Yen/Dollar level. With the normal delay of 2 to 3 years from the major exchange rate change to

the change in trade balance1, around the end of 2000 U. S. trade deficit reached its

peak and the dot-com bubble of Clinton started to burst2.

China Raising; is it made in America?

Fig. 8-1 shows that the U. S. trade deficit with China has been growing very rapidly since 1989.

The U. S. trade deficit with China was about $6.2 billion versus the U. S. trade deficit with Japan

about $50 billion at 1989. By 1995 trade deficit with China had grown to $34 billion vs. $59 billion

with Japan. Such rapid growth of Chinese exports to the U. S. market certainly had pressured

the exports of other small Asian economies and had intensified the Asian financial crises.

Let us see how China has risen so rapidly to become an export dynamo of consumer goods.

Under the leadership of Deng Xiaoping China has started to emerge since 1978 from the disaster of

The Great Cultural Revolution of Chairman Mao. The People's Communes in rural area were disbanded

to restore vigor in agriculture. Many inefficient national companies were closed. Foreign direct

investments were courted to set up factories to produce inexpensive consumer goods for exports,

utilizing China's vast under employed cheap labor resource. In other words China has also followed

"Taiwan Model" to climb the economic ladder. China seemed to have all the essential conditions

required for "Taiwan Model" to work. For example, under the strong control of communist government

there were no labor unrest, plenty of under employed workers, no opposition to

industrial developments due to the pollution, no one has the right to own land

except the government so direct foreign investments can easily get lands needed to build

factories, and Chinese Yuan was pegged to the U. S. Dollar. However, U. S. trade deficit

with China simply was not visible until 1986. We start from the investigation why

China's export oriented economy failed to gather steam during the first half of 1980s.

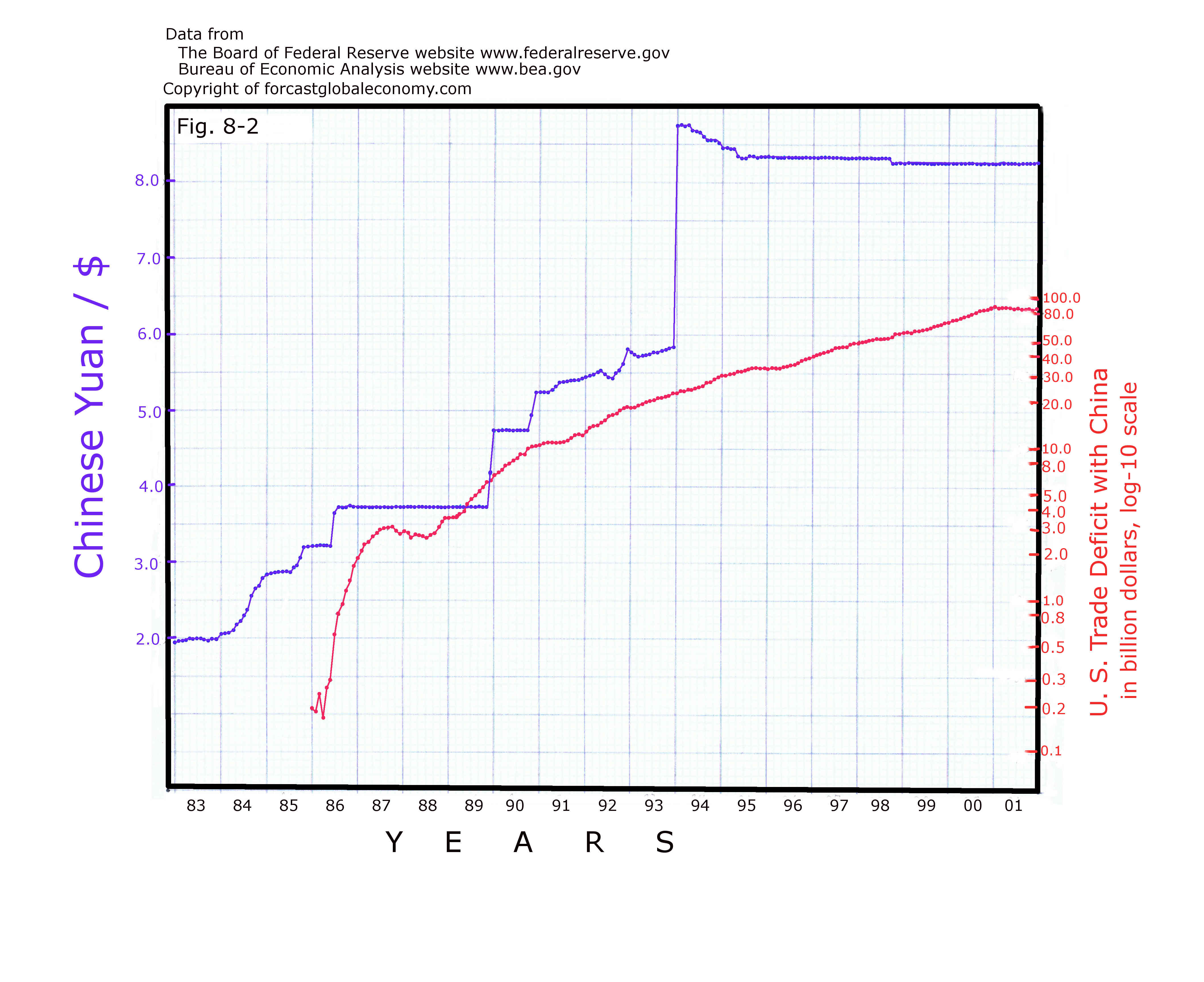

In Fig. 8-2 posted at the right hand side, the blue curve is the exchange rate of Chinese

Yuan to U. S. Dollar, expressed in Yuan/Dollar. Higher the blue dots, weaker the Yuan to

Dollar. The blue graph is plotted with monthly intervals. The data of blue dots are the midnoon

exchange rate traded at NY currency exchange tabulated by The Federal Reserve Board. Since the

actual Chinese currency are not allowed to be traded outside the country until very recently,

the quoted prices are the prices of a kind of future instrument, but the prices here reflect

closely the actual exchange rate between Chinese Yuan and U. S. Dollar; it is more than enough

to serve our purpose in this discussion. The red curve is the 12 month moving average

of U. S. trade deficit with China. The red U. S. trade deficit with China dots are plotted

using the scale of log-10( billion dollars). It is worth to note again that in a logarithmic

curve, the slope of the curve indicates the % change of the data.

In Fig. 8-2 posted at the right hand side, the blue curve is the exchange rate of Chinese

Yuan to U. S. Dollar, expressed in Yuan/Dollar. Higher the blue dots, weaker the Yuan to

Dollar. The blue graph is plotted with monthly intervals. The data of blue dots are the midnoon

exchange rate traded at NY currency exchange tabulated by The Federal Reserve Board. Since the

actual Chinese currency are not allowed to be traded outside the country until very recently,

the quoted prices are the prices of a kind of future instrument, but the prices here reflect

closely the actual exchange rate between Chinese Yuan and U. S. Dollar; it is more than enough

to serve our purpose in this discussion. The red curve is the 12 month moving average

of U. S. trade deficit with China. The red U. S. trade deficit with China dots are plotted

using the scale of log-10( billion dollars). It is worth to note again that in a logarithmic

curve, the slope of the curve indicates the % change of the data.

The exchange rate of Chinese Yuan to U. S. Dollar was set at 1 to 1 in the era of The Great

Cultural Revolution. After 1978 economic reform, the exchange rate was lifted gradually. As Fig. 8-2

shows in 1983 the exchange rate was around 2 Yuan/Dollar. This exchange rate made Chinese labor cost

too expensive to lure foreign direct investments. That was why there was nothing to show about the

U. S. trade deficit with China during the first half of 1980s. Chinese Government noticed

this problem and steadily raised the exchange rate, that is, depreciated Chinese Yuan starting

from 1984 to about 3.7 Yuan/$ by 1986. Thus the U. S. trade deficit had expanded rapidly from 1985

as the red curve in the graph shows. The Yuan exchange rate was pegged to Dollar at about

3.7 Yuan/$ from the middle of 1986 to near the end of 1989, then was brought higher and higher

(Yuan weaker and weaker) until it hit 5.8 Yuan/$ by the end of 1993. At the beginning of 1994,

another massive devaluation of Yuan brought the exchange rate to over 8 Yuan/$. Since then

Yuan has been pegged to Dollar at the rate of about 8.3 Yuan/Dollar through the right most end of

the graph, that is, year 2001. It was this relentless devaluation of Yuan that had pushed

up U. S. trade deficit with China rapidly. As shown in the previous figure, Fig. 8-1, by 2001, the

trade deficit with China has exceeded the trade deficit with Japan already.

At around 8.3 Yuan/$, Chinese currency is extremely undervalued versus U. S. Dollar. That was why

when Japan's near zero interest rate policy had boosted the value of Dollar, the value of Chinese

currency against Japanese Yen was still vastly undervalued. As the consequence

foreign direct investments did not slump and the U. S. trade deficit with China just kept

expanding through the Asian financial crises. In contrast small Asian economies did not devaluate

their currencies as aggressively as China so became the victim of the financial crises

as Japan's near-zero interest rate policy was launched in 1995.

When China buys unwanted U. S. Dollar to prevent the appreciation of Yuan or to devaluate Yuan,

Chinese Government must use newly created Yuan to buy those dollars. As China's trade surpluses

zoomed up, more and more Yuan were created and saturated China's domestic market.

Those excessive Yuan then was borrowed by local governments and the parties connected to

the powerful ones to start rampant infrastructure and real estate constructions to boost

GDP enormously. That was the secret behind the rapid rise of China as prescribed by Taiwan Model.

Some may ask why U. S. Government did not stop China to manipulate the currency to boost its trade

surplus so rapidly, otherwise China would not have risen at such an astonishing speed.

However, when we understand that the whole purpose of the globalization is nothing more than

to let the U. S. run huge trade deficits, the currency manipulation of China to make

U. S. trade deficit explode was just what U. S. Government had wanted. In that sense

we can say the rise of China is actually made in U. S. A.. As for the reason why U. S.

Government wants the U. S. to have such a large trade deficit is discussed in previous

sections2 aptly already so will not be repeated here.

Conclusions

The discussion in this section shows vividly that the foundation of the globalization scheme is to

unleash "free for all currency market manipulation" in order to create huge U. S. trade deficits to

benefit some special interest groups. In the next section we will come to the process of the self

destruction of the strange globalization scheme because the U. S. had incurred too much trade deficits.

References

1.

Article 2: YEN/DOLLAR, TRADE DEFICITS, AND THE BOOM BUST CYCLES OF USA, Chih Kwan Chen (Aug., 2003).

2.

Review Forecast Section 1,

Review Forecast Section 2,

Review Forecast Section 3,

Review Forecast Section 4,

Review Forecast Section 5,

Review Forecast Section 6

3.

Article 1: SUPER LOW INTEREST RATES OF JAPAN AND THE ANOMALIES OF THE WORLD ECONOMY,

Chih Kwan Chen (Dec., 1998)

4.

Comment 39: Taipei has lost its magic "ring"

(Feb. 14, 2007, Revised on Feb. 27, 2007, Corrections and Addendum on June 24, 2009)

Continue to the next section

Return to the previous section

Return to the title, preface and content page