Section 6: A simple way to predict the demise of bubbles and the resulting recessions

in the globalization era (Revised, February 16, 2013)

It has been pointed out in previous sections that the runaway U. S. trade deficit was the driving

force of the globalization process. After those theoretical discussions, readers will naturally

want to see some practical merits from the deep understanding about the globalization process. In

this section we will discuss one of such practical outcome especially dear to investorrs, that is,

how to foretell the demise of bubbles of the globalization era.

There is an ad hoc way of telling the burst of bubbles. A bubble is like a runaway train issuing

various distress signals. A very small number of astute observers are able to catch some of the

distress signals and foretell the burst of the bubble, though the underlying mechanism of

driving the bubble is not understood. The problem of the ad hoc approach is that no two bubbles

are alike even they both are bubbles formed during the globalization era. This means that the

distress signals vary widely from bubble to bubble, so it is very difficult for one observer to

predict the burst of bubble consistently. However, our approach based on the deep understanding

about the underlying mechanism powering all those bubbles will allow us to predict the burst of

all bubbles within the globalization era.

The evolution of U. S. trade balance and Real GDP

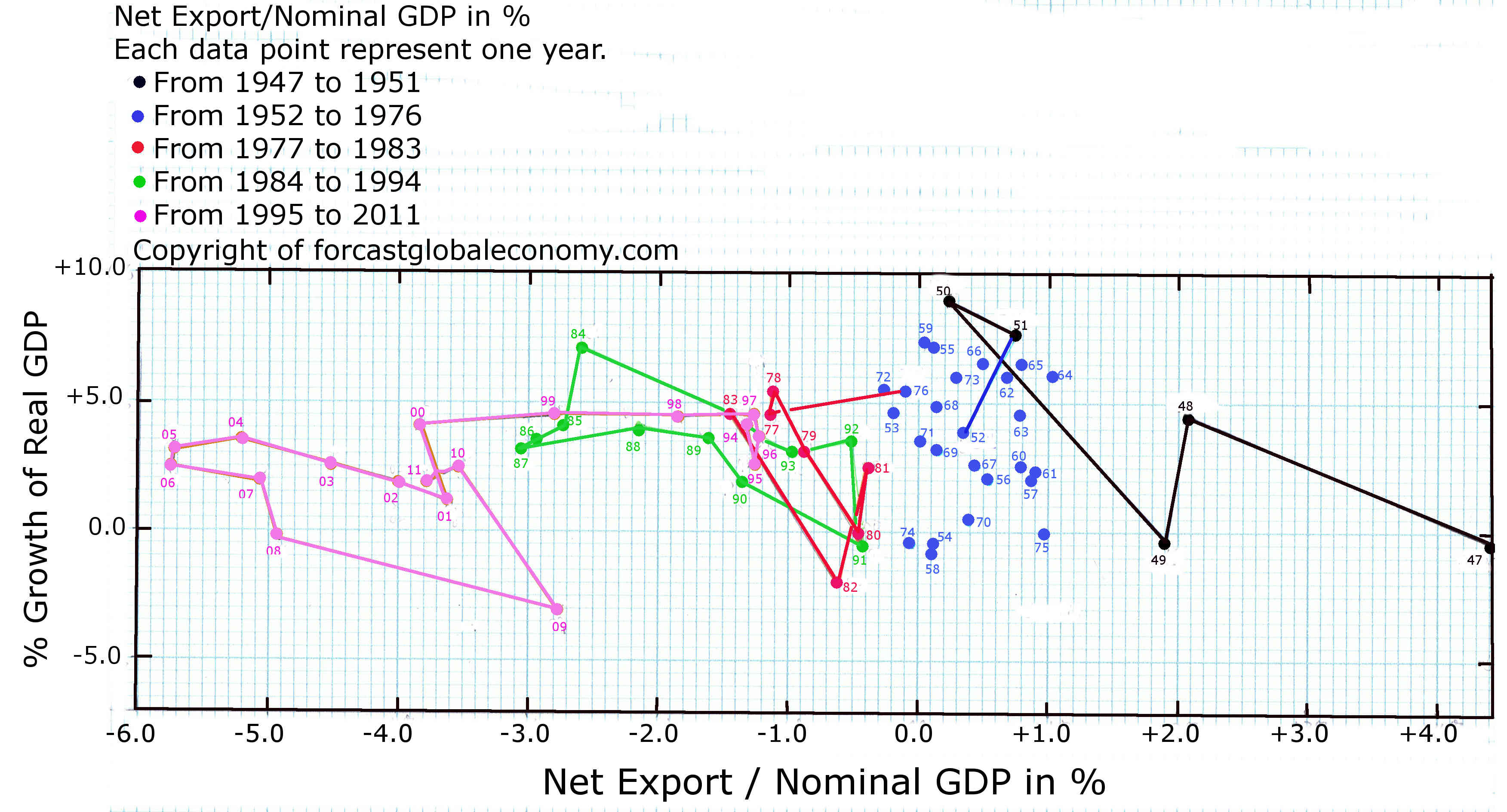

Since we are emphasizing so much about the importance of the runaway U. S. trade deficit, let us

establish a clear view first about how drastically U. S. trade balance has changed from the

pre-globalization era. In the graph at the right, the vertical axis indicates the annual % change

of Real GDP (Real means "inflation adjusted"), and the horizontal axis represents the ratio of

Net Exports over Nominal GDP expressed in %, where Net Export is the balance of trade of both

goods and services. Net Exports and Nominal GDP are not adjusted for inflation, but their ratio

allows us to ignore the effect of inflation. Each year is

represented as one dot on this diagram. The graph covers the years from 1947 to 2011. To make

the graph easy to read, all those covered years are divided into 5 color groups, they are,

from 1947 to 1951 as black dots, from 1952 to 1976 as blue dots, from 1977 to 1983 as red dots,

from 1984 to 1994 as green dots, and from 1995 to 2011 as purple dots. Beside each dot the year

of the dot is written in the corresponding color. The adjacent dots are connected with a line to

indicate the evolution of the economic situation, except among the blue dots as will be explained

later.

Since we are emphasizing so much about the importance of the runaway U. S. trade deficit, let us

establish a clear view first about how drastically U. S. trade balance has changed from the

pre-globalization era. In the graph at the right, the vertical axis indicates the annual % change

of Real GDP (Real means "inflation adjusted"), and the horizontal axis represents the ratio of

Net Exports over Nominal GDP expressed in %, where Net Export is the balance of trade of both

goods and services. Net Exports and Nominal GDP are not adjusted for inflation, but their ratio

allows us to ignore the effect of inflation. Each year is

represented as one dot on this diagram. The graph covers the years from 1947 to 2011. To make

the graph easy to read, all those covered years are divided into 5 color groups, they are,

from 1947 to 1951 as black dots, from 1952 to 1976 as blue dots, from 1977 to 1983 as red dots,

from 1984 to 1994 as green dots, and from 1995 to 2011 as purple dots. Beside each dot the year

of the dot is written in the corresponding color. The adjacent dots are connected with a line to

indicate the evolution of the economic situation, except among the blue dots as will be explained

later.

At the time when the economy cools down, idle production capacity will

be shifted to export, whereas imports will decline due to the lackluster domestic consumption.

This means that the trade balance tends to shift toward positive as the growth rate of Real GDP

declines. On the other hand, as the growth rate of Real GDP turns up, more production capacity

is geared for the domestic consumption so less for exports. Also booming economy means more

buying of foreign made goods. Thus, the trade balance will shift toward negative as the growth

rate of Real GDP turns up. This trend is called "the natural trend of trade balance".

The black dots in the graph that covers years from 1947 to 1951 is a good example of this

"natual trend of trade balance". After WWII, substantial portion of the production capacity

geared for the war effort became idled whereas civilian usage could not pick up the slack

quickly enough, so the U. S. economy fell into a deep recession with a lot of idled production

capacity. On the other hand The U. S. that had escaped the direct destruction of the war had

become the defacto factory of manufacturing to supply needed material and machinaries to devastated

Europe. As the result the U. S. trade surplus surged. As the civilian part of the U. S. economy

picked up the pace of growth while Europe had started to reuild and rebound, more production

capacity in The U. S. had turned to satisfy the domestic demand. As the result, U. S. trade

surplus declined and the growth rate of Real GDP surged. By this way a "natural trend" of the

trade balance was formed during the years from 1947 to 1951 as the black dots indicates.

The blue dots, covering the years from 1952 to 1976 are confined in the region of the horizontal

position from -0.3% to +1.1%. There is no noticeable correlation between the growth rate of

Real GDP (represented by the vertical axis) to the ratio of Net Export over Nominal GDP

(represented by the horizontal axis) so connecting lines between adjacent dots are not drawn

to avoid confusion. This means that during this lengthy period of the pre-globalization era,

the U. S. economy was more or less self-sustained and the international trade had not played a

big role in influencing the economic cycle. It was during such a condition, many modern economic

models have been constructed and rightfully ignored the trade with other countries in the first

order of approximation. Unfortunately such economic models have been directly applied to the

globalization era, still ignoring the all important factor of the runaway trade deficit.

This ignorance of the impact of the runaway trade deficit

has become the bane of those modern economic models so they have failed miserably to explain and

foretell major economic events in the globalization era. The data of 1974, near the end of this

blue dots era, represents the time of the first energy crisis. Due to Arab embargo, the gasoline

price shot up suddenly and induced a recession. Thus the trade balance tilted toward deficit

while the growth rate of Real GDP plunged. This is clearly against the "natural trend of trade

balance". However, this event was under a special circumstance influenced by non-economic

conditions. Actually when the oil embargo ended in 1975, trade balance returned to positive

though the growth rate of Real GDP stayed at negative region. Then as the growth of Real GDP

bounced back strongly in 1976, the trade balance tilted toward negative rapidly, fulfilling

the natural trend of trade balance. From there the economy entered a new phase represented

by red dots in the correlation graph.

Carter Administration, started in 1977, tried to sustain the high growth rate of Real GDP

by printing substantial amount of money. At the time when tariff had not been lowered

drastically, this money printing campaign had increased trade deficit only by a moderate

amount, but triggered a wave of high inflation instead. In 1979 the growth rate of Real

GDP had slumped under the galloping inflation, and in 1980 the economy slid into a

recession. During the slide down of the economy the trade deficit had shrunk

substantially, following the natural trend of trade balance. It is interesting to observe

that Shah of Iran had fallen in early 1979, and Iran-Iraq war that reduced the export of

Middle East oil substantially had started in 1980. As the result oil price more than

doubled compared to the level before 1979. Nevertheless trade deficit rather shrank than

increased. In 1982 U. S. economy slid into recession again. Through that period we must

conclude that the inflation, mainly due to the wanton money printing, played a major role

in dictating the economic cycle. As the inflation calmed down under the harsh monetary

restrain imposed by Volcker FED and the economy recovered, the trade deficit exploded toward

1983 and 1984, since by that time the globalization era had dawned and the tariff restrain

weakened.

From 1984 to 1994 the yearly data are represented by green dots. The growth rate of Real

GDP had continued to drop from 1984 to 1987, but the ratio of Net Export to Nominal GDP

just kept expanding toward the negative territory. This feature is totally against the

natural trend of trade balance so cannot be explained by the outdated economic models

that down play the significance of the runaway trade deficit. From 1987 to 1989, the

ratio of Net Export to Nominal GDP moved back toward positive territory but the growth

rate of Real GDP did not drop by any meaningful amount, again a feature defies

the natural trend of trade balance that cannot be explained by the

outdated economic models. Only from 1989 to 1991 the natural trend of the trade balance

was restored as the economy slid into the recession of 1991. The failure of

the outdated economic models will be shown is due to the sea change in the underlying

economic environment, that is, the runaway trade deficit had become the dominant

force to shape the bubbles and their demises.

The data points for the years from 1995 to 2011 are all represented by purple dots.

Again there are vigorous movements of the ratio of Net Exports to Nominal GDP but with

scant movement of the growth rate of Real GDP. Just like the case described in the

previous paragraph, those movements were due to the creation and the demise of bubbles

based on the runaway trade deficit so cannot be understood by the outdated economic models

that do not incorporate the significance of the runaway trade deficit.

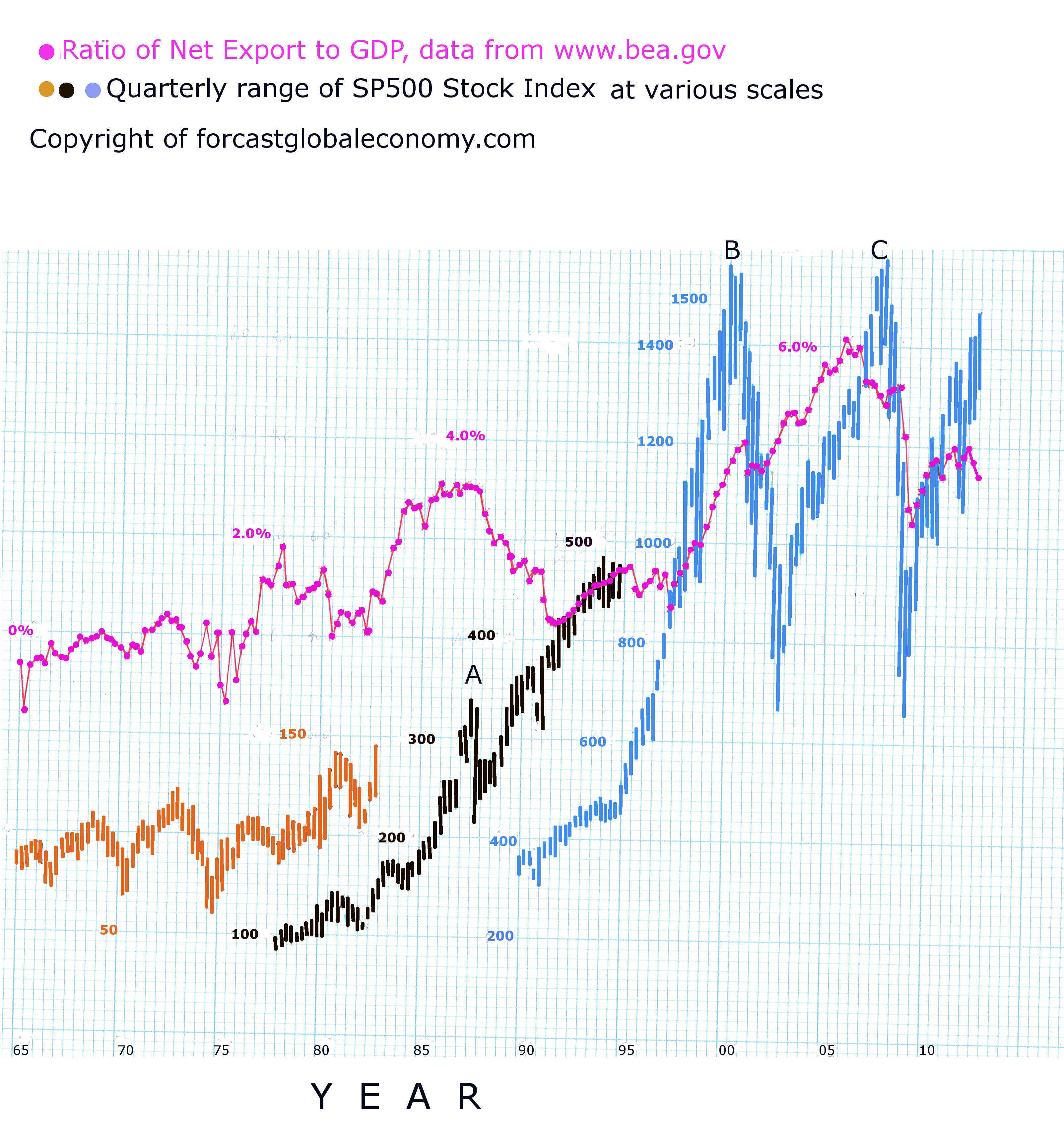

The runaway trade deficit and the bubbles

Throughout the globalization era, there had been three bubbles and their bursts. They were,

Reagan's junk-bond bubble, Clinton's dot-com bubble, and Bush's mortgage and housing

bubble. Clinton's dot-com bubble was a direct stock market bubble. Reagan's junk-bond

bubble was indirectly connected with a stock market bubble. Even in Bush's mortgage

and housing bubble that was not a stock market bubble, stock market had still played an

associative role. Therefore, it is instructive to look into the behavior of the stock

market in comparison with the runaway trade deficit, since the stock market is the

darling of Wall Street speculators that had played such a central role in the

globalization process as discussed before.

In the second graph of this section at the right, the quarterly values

of the ratio of Net Export to Nominal GDP from 1965 to 2012 are plotted as purple curve.

The quarterly high and low points of SP500 stock index are connected with a vertical

line. Since SP500 stock index had moved from below 100 at 1965 to over 1,500 at its high

at 2007, SP500 index is presented in three groups with different scales and in

different colors. SP500 stock index from 1965 to 1982 are plotted with expanded

vertical scale in red color. SP500 stock index from 1978 to 1994 is plotted with

modestly expanded scale in black color, and the stock index from 1990 to 2012 in the

regular scale in blue color.

The graph in the black bar portion shows that from 1983 to 1987 peak (labeled as black

A), SP500 index had risen from around 100 to 340 when the purple trade deficit curve

jumped enormously. Then when the trade deficit had started to fall, the stock index

fell sharply, too. The fall of SP500 stock index at black "A" is no other than the

infamous 1987 stock market crash. This shows that the 1987 crash was the burst of

Reagan's junk-bond bubble but was not a random event claimed by many analysts. The

role of computer based trading was to compress the downward move into a few days

instead of a few weeks. The subsequent rise of the stock index and the eventual

delayed arrival of a recession in 1991 will be explained in detail in Section 7.

The demise of Clinton's dot-com bubble as represented by the giant fall of SP500

stock index from the peak labeled as blue "B". The demise of the stock market

again coincides with the wane of

trade deficit as shown by the purple curve. The demise of Bush's giant mortgage

bubble had started in 2006. The first fire storm had occurred in August of 2007.

The wane of the trade deficit as shown in the purple curve had occurred in late

2006, too. The fall of SP500 stock index was delayed until late 2007 as marked

by the blue "C". The reason of this delay was due to the fact that Bush's

mortgage bubble was not a stock market bubble, so stock traders were in a dream

that China was going to save the global economy, though the giant mortgage

bubble had started to collapse already. The detailed evolution of Clinton's

dot-com bubble and Bush's mortgage bubble will be discussed in detail in

Section 8 and Section 9 respectively.

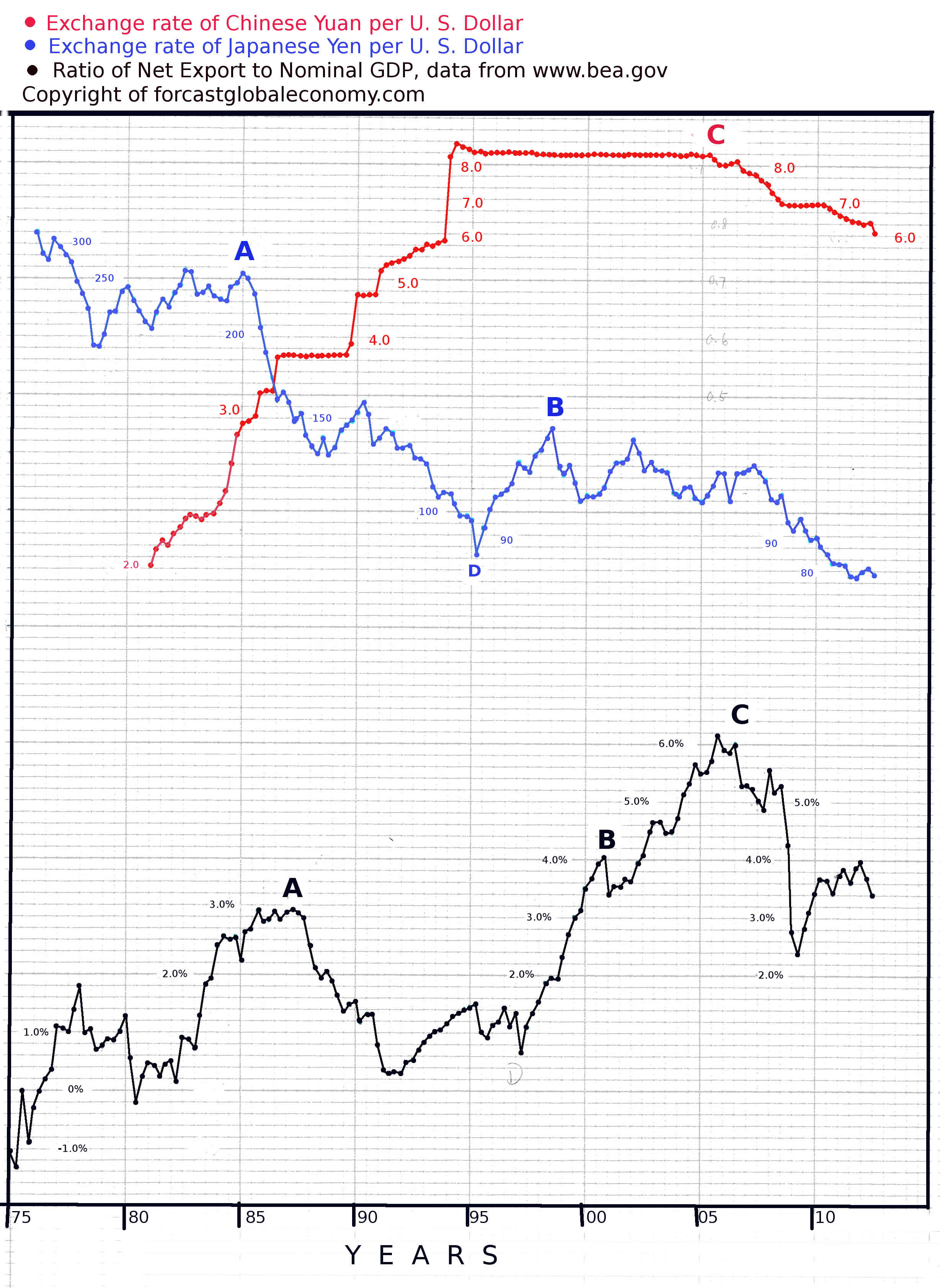

A simple way to foretell the demise of bubbles of the globalization era

After establishing connection between the wane of the runaway trade deficit

and the demises of

bubbles in the previous sub-section, clearly the way to foretell the demise

of bubbles is to foretell when the runaway trade deficit will peak. To do this

we refer readers back to

Section 2 about the relations between Dollar exchange rate and the trade

deficit. In the third graph of this section posted at the right, the now

familiar quarterly ratio of Net Exports to Nominal GDP is plotted as the black

curve. The Dollar exchange rate vs. Japanese Yen is plotted as the blue curve,

and Dollar exchange rate vs. Chinese Yuan as the red curve respectively.

During Reagan's junk-bond bubble, Japan was the major contributor to the

runaway trade deficit. According to the blue curve, Dollar had started to plunge

vs. Japanese Yen from the early part of 1985. Just add 2 to 2.5 years, that is, at

1987 the runaway trade deficit will wane. Actually the black

curve does show that the runaway trade deficit did wane at the latter half of

1987 as the peak at black "A" manifests. One may ask why 2 to 2.5 year delay? Foreign

exporters are not going to roll over just because the news that Dollar starts to

plunge comes in. Foreign exporters will try to cut cost and tolerate lower profit

margins to hang on to the market share in The U. S.. Only when Dollar plunges

relentlessly, finally foreign exporters will be forced to reduce their production

capacity and thus

the U S trade deficit will start to wane. From our experience (see Ref. 1), for the

exporter of high end consumer goods and autos like Japan, the average time delay

from the major movement of currency exchange rate to the manifestation on the

trade balance is roughly 2 to 2.5 years.

Clinton's dot-com bubble was generated by the runaway trade deficit as Dollar

soared against Japanese Yen from 1995 due to Japan's near zero interest rate

policy (Ref. 2). We should note that the rule of 2 to 2.5 year delay operates

here, too. Indeed U. S. trade deficit had started to run away again in 1997. However,

at the middle of 1998, Dollar had started to plunge vs. Japanese Yen. Then using

that 2 to 2.5 year delay rule, we can easily predict the demise of Clinton's

dot-com bubble would happen at the time period from the middle to the end of 2000.

The actual fact, shown at black "C", proved the accuracy of this prediction.

China had devalued its currency, Yuan, vs. Dollar by a substantial amount, in steps,

from 1989. Thus China has plunged into the road to become the "factory of the world" with

strong help from "Taiwan Merchants". U. S. trade deficit vs. China grew steadily

through 1990s since Yuan fixed at the level above 8 Yuan per Dollar was vastly under valued

vs. Dollar. By the end of 1990s, U. S. trade deficit against China had almost

caught up with U. S. trade deficit against Japan. At the time the drama of Dollar

vs. Yen and the wane of U. S. trade deficit vs. Japan was playing out in 2000, U. S.

trade deficit against China was still growing rapidly. That was the reason why the fall

of U. S. trade deficit after the plunge at peak "B" was rather shallow. As U. S. economy

started to recover in 2002, U. S. trade deficit against China just grew further and

further. At that time China had already taken over Japan as the major contributor

to the runaway U. S. trade deficit. At 2005, under the pressure from U. S. Congress,

China was forced to let Yuan appreciate gradually vs. Dollar. China's exports

are mainly lower profit margin products compared to Japanese exports. Thus the time

delay from the movement of Yuan to the impact on trade will be shorter than the case

of Japan. We put the time delay at 1 to 2 years. Indeed by the end of 2006, U. S.

trade deficit had started to turn down and Bush's giant mortgage bubble had started

to unravel. The first explicit sign of implosion of the bubble had appeared in

August of 2007 when the commercial paper market closed the door to speculators

playing mortgage backed securities. As mentioned before, Bush's giant mortgage

bubble is not a stock market bubble, so stock market players had continued to

indulge in the fantasy like "decoupling theorists" that China, the super economic

power(?) of the world, will come to the rescue even The U. S. falls into hard time,

so U. S. stock market continued to rise. That kind of false arguments had confused

many investors so the stock market held up until late 2007 in spite of the obvious

sign that the mortgage bubble was unraveling.

In concluding this section, we discuss our record of predicting the demise of

bubbles in the globalization era here. This line of research that has uncovered the

runaway U. S. trade deficit as the driving force to control the generation of

bubbles and their demises has started in 1997 and bore fruit in 1998. At

December of 1998, the first paper in English (Ref. 2) was posted on a personal

webpage of Prodigy. In the paper it is predicted that Clinton's dot-com bubble

will burst in the summer of 2000 based on the argument presented already. We

followed our own advice and got out of all high tech stocks by the summer of 2000

so have escaped heavy losses. Near the end of 2005, another article (Ref. 3)

has been posted on our website,

www.forcastglobaleconomy.com. Ref. 3 was to assure that no recession would occur

within 12 months from the end of 2005, but said that if a recession should come,

it will be in 2008 based on the movement of Chinese Yuan as discussed above.

In 2007, following our own advice again, we started to monitor economic data

with added vigilance in order to locate any sign of the approaching (predicted)

recession. In Ref. 4 posted at the beginning of August, 2007, a recession watch

was issued. Then in March of 2008, a stronger warning about the recession was

issued in article 10 (Ref. 5). Of course, the research is not able go back in time

and predict the demise of Reagan's junk-bond bubble. However, by applying the

research result to Reagan era, we have discovered that the 1987 stock market

debacle was not a random event but indicated the demise of the Reagan bubble. Also

the peculiar behavior that the stock market bounced higher after the debacle and

the economy had slid into a recession in 1991, four years after the burst of the

bubble, can now be explained successfully as will be shown in the next section.

References

1.

YEN/DOLLAR, TRADE DEFICITS, AND THE BOOM BUST CYCLES OF USA, Chih Kwan Chen (Aug., 2003)

2.

SUPER LOW INTEREST RATES IN JAPAN AND THE ANOMALIES OF THE WORLD ECONOMY,

Chih Kwan Chen (Dec., 1998)

3.

Comment 25: Is a recession looming? 3. The power of imports to boost GDP. Conclusion: A recession is not likely within next 12 months.

(Oct. 18, 2005)

4.

USA Outlook Update (July 28, 2007, a new graph added on Nov. 7, 2010): A Recession Watch! Massive downward revisions in the 2nd Quarter (2007) GDP report paints

a much weaker US economy than we have perceived.

5. ANATOMY OF ECONOMIC BUBBLES:

US economy from 1960 to 2007, Chih Kwan Chen (March 6, 2008)

Continue to the next section

Return to the previous section

Return to the title and content page