Quantitative Easing, abbreviated as QE, originally means for FED to create money by buying U. S. Treasuries either in the secondary market or from the primary auctions. QE is considered to be a very aggressive means for FED to create money. In the normal times this distinction between QE and the normal process of money creation is proper. The most dominant way for FED to create money is for FED to enter the overnight-interbank-market to inject money by buying up U. S. Treasuries from participating banks with dollar credits; the operations carry the agreement that the banks will buy back the U. S. Treasuries next day so it is called “overnight repurchase agreement”. By performing such “repurchase agreement” continuously and in the expanded way, FED can inject money into the economic system. Another way for FED to inject money is to allow needy banks to borrow from FED through the “Discount Window”. The borrowing from FED's Discount Window is also overnight loans and the borrowing bank must put up highest rated debt instruments, usually means U. S. Treasuries, as collateral for the loans. Compared to those overnight transactions, QE at those times had significantly different impact. Even if Fed just purchases 3 month T. Bill, it means that FED has injected money for three months, not just overnight, and thus can expand the amount of money flowing through the society drastically.

However, after the 2008-2009 crash, such stringent definition of QE has lost meaning. For example, the duration of Discount Window borrowing has been extended to 3 months, and FED had started the auction of loans with 3 month maturity under a program called “term auction facility”. And then Fannie Mae and Freddie Mac have been nationalized and FED eagerly bought debt instruments issued by them. For the loans, FED has accepted all kinds of junks as collateral and even today it is refusing to disclose in full what kinds of junks it had accepted as collateral under the panic of the crash. As the effect of creating and injecting money into the system, the distinction between the ordinary monetary operation and the old-kind definition of QE has blurred to the degree to make it meaningless. Thus here QE just means abnormal phases of money creation.

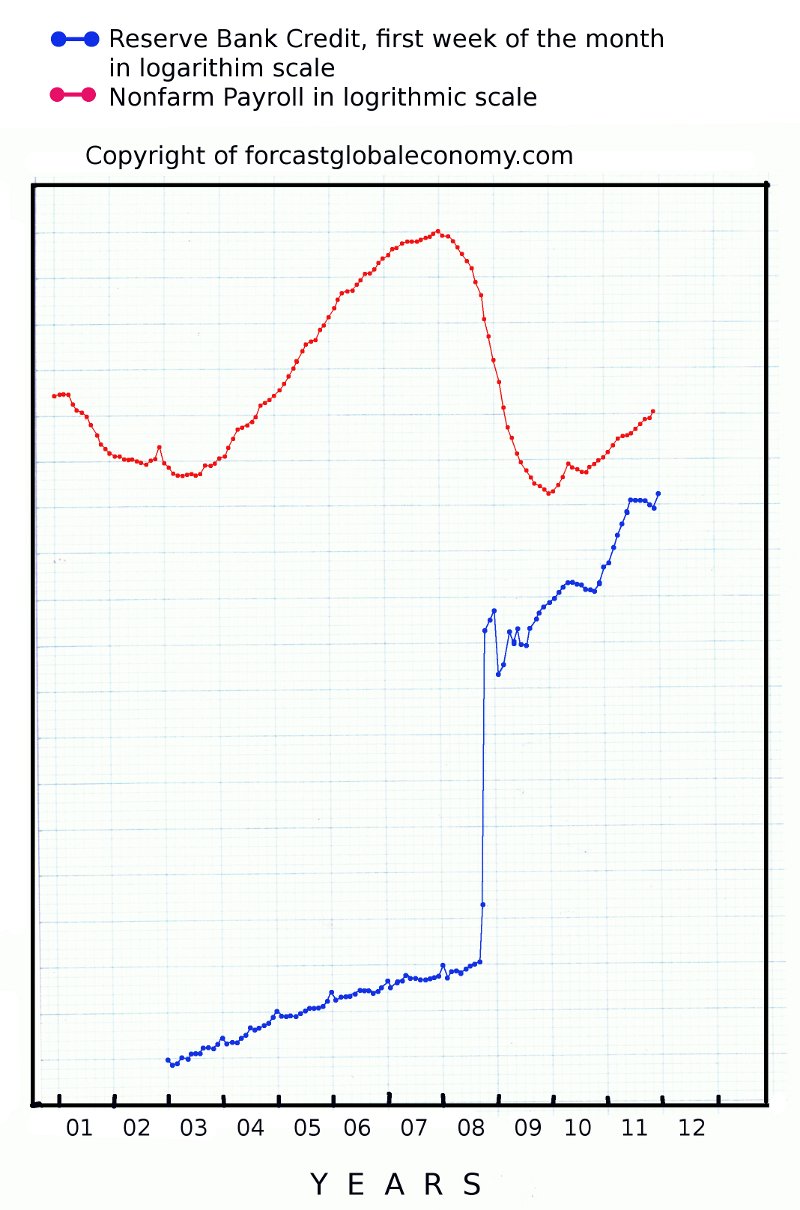

To spot QE, the abnormal phases of money creation, it is best to look at the total amount of money created by FED itself. FED publishes its balance sheet every week. Among the balance sheet items, there is a number called “Reserve Bank Credit”. That item indicates exactly how much money has been created by FED but is still outstanding. Since it is too much to plot Reserve Bank Credit in the interval of every week, the number at the first weekly release of every month is plotted in logarithmic scale as the blue curve in the graph at the right; the date covered in the graph is from January, 2003 to January, 2012.

From the graph we can see that the blue money creation curve jumped suddenly between the beginning of September, 2008 and the beginning of October, 2008. The sudden jump followed the collapse of Lehman Brothers and the ensuing panic thereafter. However, this does not mean that the whole financial crises had started at the sinking of Lehman Brothers. The first financial firestorm had hit in August of 2007 already as the commercial paper buyers boycotted against investment vehicles speculating on subprime mortgage backed papers. Then came the panic of financial institutions in securing liquidity at the end of 2007, the sinking of Bear Stern in the spring of 2008, and followed by the collapse of Fannie Mae and Freddie Mac in the summer of 2008. Only FED was not aware of the consequence of the successive financial firestorms and had responded with normal monetary easing, not with QE. It was the collapse of Lehman Brothers that finally woke FED up to the calamity and forced it to undertake the first phase of Quantitative Easing (QE1) in panic. After a period of uncertain footsteps of FED until the fall of 2009, as manifest by the gyration of the blue money creation curve, QE1 had sailed into a calmer water and had continued until the late spring of 2010.

The red curve in the graph is the monthly nonfarm payroll number plotted in the logarithmic scale. Comparing the blue money creation curve with the red job creation curve, we can see that QE1 had arrested the decline of the red job curve by the winter of 2009 to 2010, and then pushed it up through the spring of 2010. However, as QE1 came to the close around the late spring and the early summer of 2010, the red job curve started to slacken again. The deteriorating job market then prompted FED to start QE2 at November of 2010. QE2 then pushed up the red job curve again. The temporary stagnation of the red job curve in May and June of 2011 probably was due to the impact of Japan's great earthquake. Ironically as Japan rebuilds from the disaster, the demand of instruments and material for reconstruction probably has added fire to U. S. manufacturing. This demand from Japan in combination with the lingering effect of QE2 have caused the red job curve to rise at a steady rate since July of 2011, though QE2 has officially ended at the end of June, 2011 as confirmed by the behavior of the blue money creation curve.

Nonfarm payroll number, that measures how many people are working in the nonfarm sector of the society, is volatile near the end of a calendar year. This is due to the sudden surge of consumer shopping in the season from Thanksgiving to Christmas and retailers hire many temporary workers. Government statisticians try to correct such seasonal variation and uncover a true trend of nonfarm payroll number by consulting with the pattern of swing of past years. In 2010 retailers were still gripped by the stigma of the crash and were very cautious in adding temporary workers during the Christmas shopping season, but during the past Christmas season they were more upbeat in adding temporary workers. This kind of trends will make seasonally adjusted nonfarm payroll number artificially inflated in November and December but the number may experience a sudden drop in January. Thus we need to wait for a while to make sure that the steady uptrend of the red nonfarm payroll curve is the real thing. If it is the real thing, then it is dangerous for FED to undertake QE3 at this point. We will see why it is so next.

The economic activity is the product of total amount of money created multiplied by the speed of the flow of money through the society, called the velocity

of money. Let the economic activity of a society be represented as G, the amount of money M, and the velocity of money V. We can write an equation

G = M • V ,

(1)

where “•” means multiplication. Since G, M and V are all functions of time t, simple calculus says that the rate of change of all three quantities

can be expressed as differentials by time t, (dG/dt), (dM/dt) and (dV/dt) respectively. Then comes the following equation

(dG/dt) = V • (dM/dt) + M • (dV/dt) . (2)

Suppose we are in a period that M is kept steady, so (dM/dt) = 0. The above equation (2) becomes

(dG/dt) = M • (dV/dt) .

(3)

This relation means that the growth rate of the economy, (dG/dt) is proportional to the growth rate of the velocity of money, (dV/dt), with the amount of

money M serving as the coefficient. At a situation that M is very large, like in the current situation, a small pick up of the velocity of money, that is,

a slight increase of (dV/dt) is going to cause outsize increase of (dG/dt), the economic growth.

The bubble of 2003 to 2007 was a debt bubble. As the giant debt bubble collapsed during the period from August of 2007 to the middle of 2009, lending and borrowing activities fell sharply. As the result the velocity of money, V, shrank and had caused the plummeting economic growth rate (dG/dt). In order to counter the drop, FED created a lot of money through QE1 and QE2 to counter the economic decline. That is, in the equation (2), (dM/dt) is increased to counter the negative (dV/dt). To understand what kind of (dM/dt) we are talking about, we should note that before September of 2008, Reserve Bank Credit, the blue curve in the graph, was kept below 900 billion dollars. After QE1, at November of 2010, Reserve Bank Credit, or M at that time, was 2281 billion dollars, that is more than doubled compared to the pre-panic level. QE2 had added another 500 billion dollars to Reserve Bank Credit that stood at 2798 billion dollars at December, 2011. We can see that just QE1 and QE2 have already pushed the economy into a very dangerous situation of exploding economic growth later unless the velocity of money never rises again. If the velocity of money, V, rises even by a modest amount, it will be translated into a rapid growth rate of the economy, (dG/dt) from Equation (3) due to the huge size of M. If FED tries to reduce M rapidly to prevent the development of another huge bubble, than the short-term interest rate will rise rapidly ahead of the long-term interest rate, creating a situation of inverted yield curve that is a precusor of an incoming recession. If FED fails to withdraw money fast enough to counter the rising velocity of money, then the bubble will get out of hand. As such giant bubble burst inevitably, the global economy will certain to be pushed into a depression. Under such consideration, it is ill advised for FED to undertake QE3 at this stage since it will only inflate M further and creates a more dangerous condition. Even if the red nonfarm payroll curve in the graph starts to go sideways, FED should be refrained to undertake QE3 since it will be like to drink poison to ease thirst, unless FED is absolutely sure that the velocity of money will never increase again.

The blue money creation curve in the graph had jumped suddenly from December, 2011 to January 2012 by about 100 billion dollars. About 50 billion dollars are due to the currency swap as discussed in Comment 85. The process is for ECB to borrow U. S. Dollar from FED and auction those dollars to needy European banks. As the result the interest rate of borrowing dollars in London Inter Bank market has not only stopped rising but has trending down recently. The remaining 50 billion dollars are the year end effect and should dissipate in January. As discussed in Comment 85, SWAP to save European banks may be used as a back door QE3. We shall see whether FED will drain away the dollars created during the SWAP and let Reserve Bank Credit to fall back to early December, 2011 level to prevent the SWAP turning into a back door QE3, or not.