The crises of Euro is continuing in spite of the expanded efforts to help Greece. Many are confused by the sovereign debt crises of Europe with the budget deficit problem of The United States of America. When the Euro crises is in the mind of the markets, stock prices dive but U. S. Dollar and the prices of U. S. Treasuries jump. When U. S. budget deficit becomes the concern, U. S. Dollar and the price of U. S. Treasuries should come down along with stock prices. Current strong up trends of U. S. Dollar and U. S. Treasuries imply the recent gyrations of the stock prices are due to the continued worry about Euro crises, but not about U. S. budget deficit even with the failure of The Super Committee to agree on the ways to reduce the budget deficit.

Many will ask how do the sovereign debt crises of Euro region differ from the seemingly huge U. S. budget deficit. The differences is due to the polarization effect of Euro to make the winners' trade surpluses explode and the losers' trade deficits run wide as has been pointed out in Comment 83, using Germany and Greece as the example. U. S. governmental budget deficit, though is huge, does not pose an imminent threat because U. S. retains its power to manage its own currency. The ins and outs of U. S. budget deficit will be discussed elsewhere. In this article we will continue to consider the Euro crises. In Comment 83, we only demonstrated the cases of trade balances of Germany and Greece. However, many other Euro region countries can also be categorized as winners or losers with regard to their trade balances. Here we will expand the coverage to those countries.

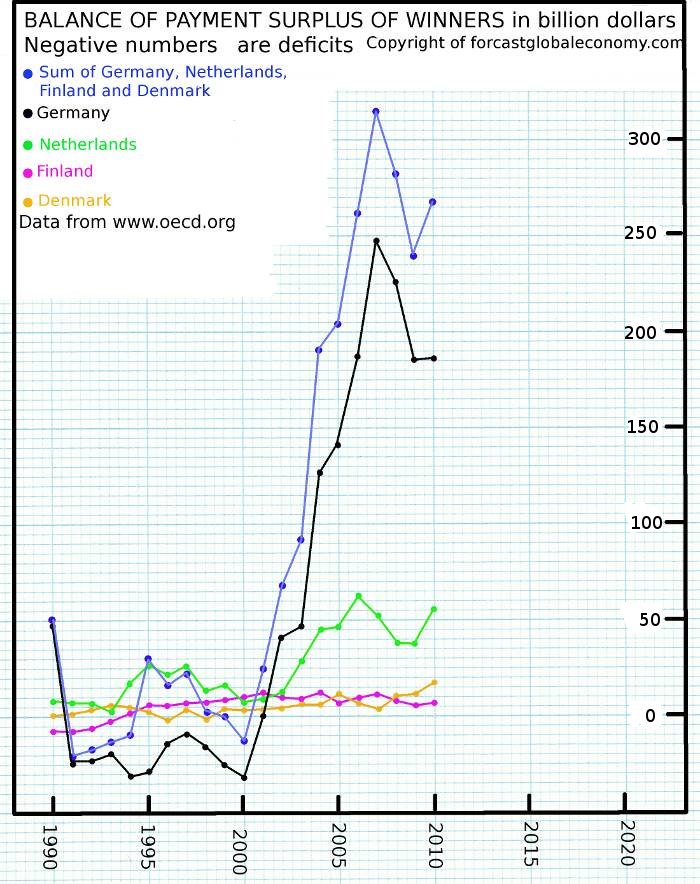

| In the first graph at the right, balance of payment surpluses of Germany, Netherlands, Finland and Denmark are plotted with various colors, in unit of billion U. S. dollars. Positive numbers are surpluses and negative numbers are deficits. The blue curve is the aggregate sum of the balance of payments of those four winning nations. Germany is by far the biggest winner, implying that by pegging to Euro, German Mark becomes vastly undervalued compared to the case of a standing alone Mark. Netherlands is the distant second winner with its currency moderately undervalued compared to the case of not joining Euro. The currencies of Finland and Denmark in case of not joining Euro, is at par value with Euro. |

|

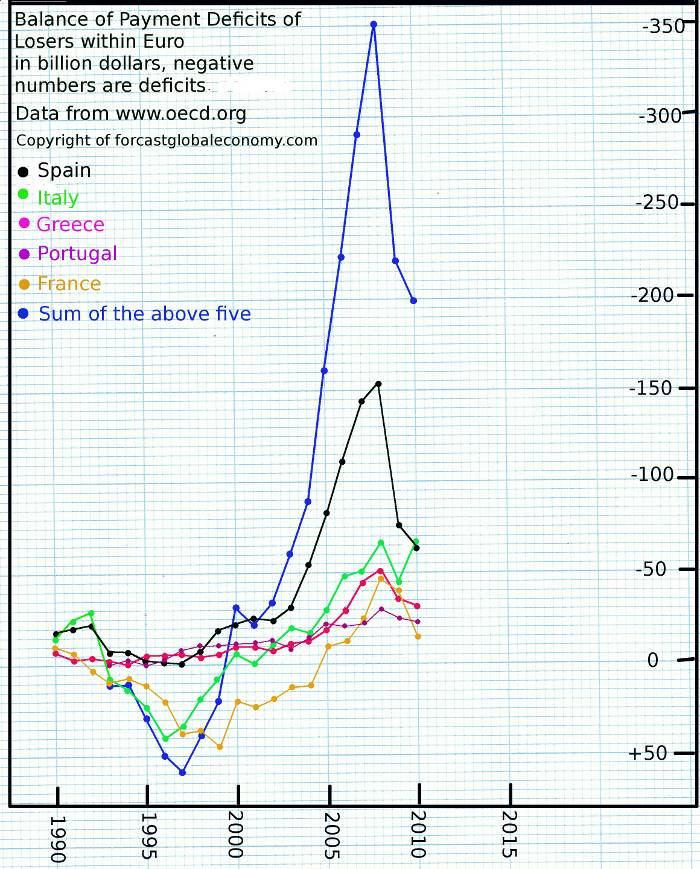

| Balance of payment deficits of Spain, Greece, Portugal, Italy and France are plotted with various colors in the second graph at the right. Negative numbers in the unit of billion dollars are deficits and is plotted as the deficits increase going north. Positive numbers are for surpluses, but the surplus increases as going south. The blue curve is again the aggregate sum of the balances of those five countries. |

|

The aggregate trade surpluses of the winners in the Euro-region, that is, the blue curve in the first graph is roughly synchronized with the aggregate trade deficits of the losers, the blue curve in the second graph. This result is due to the fact that a currency union like Euro is actually a kind of currency manipulation. It makes the currencies of the winners undervalued so that their trade surpluses will unduly explode, whereas the currencies of the losers become overvalued so that their trade deficits will be enhanced. As has been pointed out in Comment 83, when a loser country runs balance of payment deficit, the originally allocated Euro flows out of the country. If similar amount of Euro is not borrowed from the outside, the currency in circulation of that country will be depleted and its economy will spiral down into an abyss. However, with the existence of Euro, the loser is bound to keep running the balance of payment deficit and will require the borrowing from outside year after year without the end in sight. This kind of ridiculous situation created by Euro, of course, cannot continue for long and then the crises when the lending from the outside dries up.

To force the loser government to cut its budget deficit at the time of economic distress apparently will only make the situation worse. When an economy is in distress, government expenditure will increase due to the social safety net. The government must borrow a lot of money and distribute them to the needy. If the government cut back the aid then the personal income of the society will plunge, consumption dwindle further, businesses shrivel more, the government receive less tax revenue and the budget deficit will widen more. The attempt to revamp the underlying structure of the society to gain more productivity take a long time to be done. The short-term damage due to the attempt to cut the governmental budget deficit will overwhelm the long-term potential gain, and thus the crises will only deepen.

We should know that the polarization effect of Euro remains even all the loser countries leave Euro. Then Finland and Denmark will become losers to substitute the winner, Germany and those two countries will fall into crises just like the current losers. If Finland and Denmark also leave Euro at the end, then Netherlands will become the loser. In other words, Euro is destined to disintegrate.

Some argue that a stronger financial integration will save Euro, but that is just an illusion. Those people may point toward The United States as a guide. However, they should understand that in The United States the main burden of social safety net spending like the aid to the needy and unemployed is picked up by the central government, and is uniform through out the whole country. Each state only plays an auxiliary role on that front. Also there is no restriction to prevent people to move from one state to another. If unemployed and distressed people in Greece are free to move to Germany, and are allowed to collect unemployment compensation and welfare aid from German Government instead of from cash strapped Greek Government, then the Greek crises will be solved. Without the determination to go to not just a financial but a total political union quickly, the chance for Euro to survive is indeed very slim.